I posted an abbreviated list of “Stocks to Watch 2020” on January 1st prior to completing my detailed analysis but now it is complete and pasted below. All stock prices quoted are from January 1, 2020.

I received questions on social media asking why I didn’t include the FAANG stocks and other big-time names that normally dominate the headlines. The annual “Stocks to Watch” list typically includes new and up-coming growth stocks that I own or candidates I am looking to own. Stocks such as AAPL, AMZN, GOOGL, MSFT, FB, V, MA, etc. should be owned in almost every portfolio already, whether in your active trading account or a more passive retirement account. Own those stocks as they will all likely double or triple over time, once again. Own an index fund as well and add dollars to it annually, during up and down years – just do it and check back in 30 years.

Honestly, 95% of all folks should just own index funds and call it a day and forget about trading or investing in individual equities.

My annual blog post, Stocks to Watch, targets equities that I trade within my active trading/investing account, an account that’s smaller and more active than my conservative accounts (retirement, index and company stock). I don’t disclose the number of shares or the size of the account as that’s personal information. What I will disclose, here and on twitter, is what I own, what I buy and what I sell. I do believe in being transparent with the equities I hold as well as the equities I don’t when discussing them on the blog or social media.

As some term it on Fintwit: “Skin-in-the-Game”.

I like that because I love the book “Skin in the Game” by Nassim Nicholas Taleb.

I don’t trade for a living nor do I aspire to trade for a living. I invest to increase my overall net worth and to “play the game”. I do get a thrill at trying to beat the market averages by making my own decisions. Some years this works and in others, it doesn’t.

I can hold a position for years or I can be out within days. It’s not about being right or wrong, it’s about making money and protecting capital. I’m wrong with my buys and sells more often than I am right but overall, I usually make money over the long term because I often catch a couple big time winners, which double or triple within a year or two. I am not a millionaire from investing in stocks so don’t rely on me for the answers – fintwit claims that these geniuses exist all over the place so good luck finding them (hint). My primary income and net worth is generated from my business career, which focuses on commercial real estate.

With that said, let’s jump right into it. I make a note of the equities I currently own (on this year’s list), which ones I am looking to own and which ones I am waiting for ideal setups.

Enjoy my 15 Stocks to Watch for 2020, in no special order:

-

OKTA – $115.37: Okta, Inc. provides identity solutions for enterprises and other businesses, serving in the security software sector, along with companies such as PANW and CYBR. Sales have been increasing QoQ by an average of 58% the past 8 quarters, from $77.1MM to $153.0MM for a total gain of 98%. The stock debuted as an IPO on April 7, 2017 yet institutional fund sponsorship has increased more than 84% over the past four quarters from 449 to 827 funds.

Experience shows stocks that enter the 500-1,000 fund level are prime candidates for additional gains. It’s not a given but I always want to be on a train with strong institutional support.

Technically, the stock made an all-time high back in July, reaching $141.85, before building its current five-month base. Shares can be accumulated now as it trades just above both the 50d and 200d moving averages. I said last year that “I see OKTA as a classic $60 to $100 mover over the next 12 to 24 months.” Well, it made that move and then some within the first six months of 2019. I can see OKTA above $200 over the next 12 to 24 months.

I am long shares of OKTA.

-

STNE – $39.89: StoneCo Ltd. provides financial technology solutions that empower merchants and integrated partners to conduct electronic commerce across in-store, online, and mobile channels in Brazil.

Borrowing my line from last year, I’ve been a big fan and holder of financial solutions and credit companies for years (i.e.: Visa, Mastercard, Square) so naturally, STNE grabbed my attention following its IPO in October 2018. Sales have increased an average of 65% per quarter (QoQ) over the past eight quarters (moving from $74.7MM to $161.1MM), while earnings are up an average of 376% the past 8 quarters (going from $0.03 to $0.17).

The stock is less than 10% from an all-time high as it continues to build the final side of its nine-month base. I wouldn’t mind a several week handle to form on this irregular shaped base before the stock looks to make a new all-time high.

Warren Buffett is one of the top holders of the stock but it could use more institutional support in order to make another double up. I like STNE to double up over the next 12+ months. Shares can be accumulated near either of the major moving averages (50d or 200d).

I am long shares of STNE.

-

ROKU – $133.90: Roku, Inc. provides a TV streaming platform and devices for entertainment.

I missed this stock in 2019 as it exploded from $26.30 to more than $176 per share (December 2018 to September 2019). Coworkers and friends were talking about “Roku” but I had my head in the sand as I wasn’t a user of the product = “you don’t know what you don’t know”.

Sales have increased a total of 38% over the past 8 quarters from $188.3MM to $260.9MM with an average gain of 46% QoQ. Institutional sponsorship is up more than 145% the past four quarters, entering that key 500-1,000 fund range.

The stock has been building a base the past four months but the company has a product and service that is as hot as anything else on the market right now so I am interested. It currently trades below the 50d ma but above the 200d ma so one can accumulate shares here, for the long term. I can see a longer base formation before a return to new highs later in 2020.

I am long shares of ROKU.

-

ZM – $68.04: Zoom Video Communications, Inc. provides a video-first communications platform (via the cloud) by connecting people through frictionless video, voice, chat, and content sharing.

My biggest crutch with ZM in 2019 was its valuation, too high. It’s still high today but the technology is first class as I use it on a daily basis. I am now interested in grabbing shares due to the six month base that the stock has formed. The stock trades 37% off of all-time highs and may be beginning to build the right side of a long base. Risk takers can grab shares here to see if this is the bottom.

Sales have increased 227% the past eight quarters with an average gain of 132% QoQ while earnings have turned positive with an 800% and 300% increase the past two quarters, as compared to the same period the prior year.

I do not own shares as of this writing but I am very close to pulling the trigger on my initial position and will post to twitter when I do.

-

LVGO – $25.06: Livongo Health, Inc. develops digital health devices to monitor chronic health conditions. The platform provides cellular-connected devices, supplies, informed coaching, data science-enabled insights, and facilitates access to medications.

The stock debuted with an IPO on July 25, 2019 and quickly fell by more than 50% in value. Bottoming in September, the stock then doubled in price by Thanksgiving before cooling off to end the year. So goes the volatility with new IPOs.

What attracts me to the stock is the innovative SaaS service with regards to the healthcare industry and their small but explosive sales growth QoQ. Sales have increased from $7.7MM in December 2017 to $46.7MM in September 2019, a 500% increase for an average of 135% quarterly. Even though sales are exploding, earnings remain negative and are projected to stay this way for at least the next year, although the loss was cut in half in the September 2019 period to -0.04, from -0.10.

The 50d ma is now trending higher so investors can start to accumulate shares here, along the moving average. The point and figure chart suggests some possible downside towards $22 so I haven’t pulled the trigger just yet but I am ready. This area seems to be a comfortable entry, longer term.

I will buy shares if it drops to the $22 range. If not, I’ll buy along the 50d ma and will advise on twitter.

-

WORK – $22.48: Slack Technologies, Inc. operates Slack, a business technology software platform that brings together people, applications, and data, as well as sells its offering under a software-as-a-service model.

I bought shares of WORK in August 2019 and had to sell for a loss by early September as I was just wrong in my timing. Unfortunately, I was playing a game of “FOMO” and paid for it but kept it to a small, reasonable loss. It happens, no big deal. I am interested again now that the stock is trading 15%-20% below my sell price but more importantly, it seems to have formed an 11-week base with a positive move above the 50d ma. Shares can be accumulated in this area for a nice longer term risk-to-reward play.

Sales have increased from $68.8MM to $168.7MM over the past eight quarters for a total gain of 145% or 114% QoQ. Institutional sponsorship is still relatively low but that’s mostly because the stock is still young with an IPO date of June 2019.

I plan re-enter this stock and will advise when I do so.

-

SQ – $62.56: Square, Inc. provides payment and point-of-sale solutions with an ecosystem that includes point-of-sale software and hardware that offers sellers to payment and point-of-sale solutions.

I’m a holder of SQ shares for a while now and lived through much of the 2019 calendar year without much excitement, share price wise. The stock has been building a sideways base for 15 months, after making an all-time high above $100 in September 2018. The stock returned 10x the prior 26 months so I understand that it has to digest those gains. However, my patience has been tested over the past six months. I will continue to hold because I believe in the company and their offerings, especially Cash App and their accumulation of Bitcoin. I have been accumulating Bitcoin throughout 2019 as well with two recent purchases in December 2019 (via Gemini).

Institutional sponsorship has gone from 714 in December 2017 to 1,102 in September 2019, a 54% increase. However, the number of funds has slightly decreased from two quarters ago, when it peaked at 1,151. Sales have averaged a QoQ gain of 46% for the past two years, increasing from $616MM to $1.266B while earnings have averaged a QoQ gain of 71% during that same time period, moving from $0.08 to $0.25. The financials look solid so I will remain patient and hold shares to see if the stock price will start a new move higher (a double up is not out of the question).

I am long shares of SQ.

-

CGC – $21.09: Canopy Growth Corporation, together with its subsidiaries, engages in growing, possession, and sale of medical and recreational cannabis. Its products include dried flowers, oils and concentrates, softgel capsules, and hemps.

I mentioned last January that CGC could trade back to $50 which it did before the end of that month and then again by May 2019. Beyond that, it was all downhill. The stock is volatile but that’s because the product is controversial and the industry is new. With that said, I see steady upside over time (I don’t know if that time is 2020 or beyond).

Sales have increased from $21.7MM in December 2017 to $76.6MM in September 2019, while peaking at $106.5MM in the March 2019 period. The increase is 252% over the past 8 quarters with an average gain of 184% QoQ. Unfortunately, the earnings are still negative and I am not quite sure when they will turn positive. Due to the product, institutions have been cautious accumulating shares as sponsorship has only increased by 36% the past four quarters. This is where I see the opportunity in the stock, with future institutional interest as earnings push towards profitability and the taboo around marijuana subsides.

Technically, the stock has been building a deep base the past eight months, losing half its previous value. It appears that the stock may be building a base/bottom the past six weeks but I believe investors have time to figure this out as the 200d ma is 50% higher than the current ticker price. As I said last year, I believe this stock will once again trade above $50 per share so one can accumulate now or wait for the bottom to confirm and a move to commence on the right side of the base.

I was long shares of CGC but sold in 2019. I plan to re-enter CGC after it confirms a bottom as I like the leader in a potentially explosive industry.

-

CRWD – $49.87: CrowdStrike Holdings, Inc. develops security solutions by offers Falcon platform, a cloud based security solution that protects workloads across on-premise, virtualized, and cloud-based environments running on various endpoints, such as laptops, desktops, servers, virtual machines, and IoT devices.

The stock debuted June, 6, 2019 and quickly doubled within two months but then joined the SaaS slide this past fall and gave back more than 50%, trading slightly above the low of the four month base. The stock is looking to re-take the 50d ma and will become a buy candidate if it does (essentially the current area of trading near $50 per share).

Sales have seen tremendous growth over the past eight quarters, increasing from $38.7MM to $125.1MM for a QoQ average of 115%. I’d like to see the company turn a profit which would help ignite the share price again.

I will be looking to add shares with a close above the 50d ma, following a three week tight base to end 2019.

-

TCEHY – $48.01: Tencent Holdings Limited, an investment holding company, providing Internet value-added services (VAS) and online advertising services in Mainland China and around the world. It offers online games and social networks across various online platforms; online advertising services, such as media, social, and display-based advertising services; and FinTech, cloud, television series and film production, and other services for individual and corporate users. The company also develops software; develops and operates online games; and provides information technology, information system integration, asset management, online literature, and online music entertainment services.

The company is a holding behemoth, owning a percent of the following companies: JD, TSLA, SEA, ATVI, SNAP, SPOT, DOYU, VIP and many others.

It has been more than 21 months since Tencent made an all-time high with the past twelve months showcasing a volatile sideways pattern. Institutional Sponsorship is light at 266 funds, surprisingly, but I attribute that to it being a Chinese holding company. However, BABA has 3,805 funds holding the stock so TCEHY has a lot of upside, in my opinion.

Sales have increased 30% QoQ the past two years, moving from $10.2B to $13.6B, massive revenue. Earnings are positive but growth has been slowing, averaging only 16% QoQ the past two years.

I am long shares of TCEHY.

-

PYPL – $108.17: PayPal Holdings, Inc. operates as a technology platform and digital payments company that enables digital and mobile payments on behalf of consumers and merchants worldwide. Its payment solutions include PayPal, PayPal Credit, Braintree, Venmo, Xoom, and iZettle products.

I started watching PYPL prior to its IPO and made mention of it in my “Stock Trends for 2015” under the heading “Digital Payments (currency) & Mobile Wallets” which highlighted the following names: AAPL, GOOG, AMZN, V, MA. I bought shares following the IPO and held until 2017 and then sold. Initially my sell looked correct as 2018 was a mostly choppy sideways trend but then it popped again in 2019 but I kept waiting for a pull back and missed the move.

Here we are trading along the 200d ma inside a five-month base which is starting to build the right side, an ideal accumulation opportunity. Sales are averaging gains of 18% QoQ while earnings are averaging gains of 29% QoQ the past two years. Institutional sponsorship has increased 31% over the same time period, currently sitting at 3,047 funds.

I will be looking to grab shares in the near term and will advise on twitter when I do.

-

MDB – $131.61: MongoDB, Inc. operates as a general purpose database platform worldwide, offering a subscription package for enterprise customers to run in the cloud, on-premise, or in a hybrid environment.

The stock debuted October 19, 2017 and took a quarter to get going but once it did, it moved nearly 6-fold from its low in Feb 2018 to its high in June 2019. The stock has been forming a six month base since making its high and appears to be maintaining support near the 200d ma, trading slightly below the line. Institutional sponsorship has increased 6-fold, along with the share price, from 87 funds to 635 funds in the most recent reporting period.

Sales have increased from $50.1MM to $109.4MM the past eight quarters, averaging 63% gains QoQ during that same period. The downside, earnings are still negative as the company struggles to turn a profit. I prefer companies with positive earnings but the subscription platform they offer really intrigues me for future sales and eventual profit.

I have been watching the stock since the summer of 2019, noting that it needs to form a decent base. Shares can be added near or above the 200d ma.

I do not own shares but it’s on this list as a possible add in 2020 as the base continues to build.

-

SNAP – $16.33: Snap Inc. operates as a camera company offering Snapchat, a camera application that helps people to communicate through short videos and images.

I’ve been a supporter and holder of social media stocks (FB, TWTR & SNAP) so adding SNAP to this year’s list shouldn’t have been difficult but I use Facebook and Twitter daily – I don’t use Snapchat. I’m also over 40 years old so perhaps I don’t qualify “to understand”.

I was hesitant to add SNAP even though I successfully made money on the stock in the past, prior to its collapse in 2018. I did not jump back on board in 2019 when it made a solid run last year but I like the current technical setup. It appears to be in the midst of a five month base, currently building the right side with its sights set on a new 52-week high.

Sales have increased from $285.7MM to $446.2MM the past eight quarters, averaging gains of 48% QoQ (50% in Sept 19, the largest reading since the Mar 18 period). Earnings are negative but knocking on the door of becoming positive in 2020. Fund sponsorship is also accelerating, jumping 192% the past four quarters with 573 funds as of December 2019.

I don’t own shares and I’m not sure if I will re-enter SNAP but I am intrigued.

-

SHOP – $397.58: Shopify Inc. provides a cloud-based multi-channel commerce platform for small and medium-sized businesses. Its platform provides merchants with a single view of business and customers in various sales channels, including Web and mobile storefronts, physical retail locations, social media storefronts, and marketplaces; and enables to manage products and inventory, process orders and payments, ship orders, build customer relationships, leverage analytics and reporting, and access financing. – the long description from Yahoo Finance.

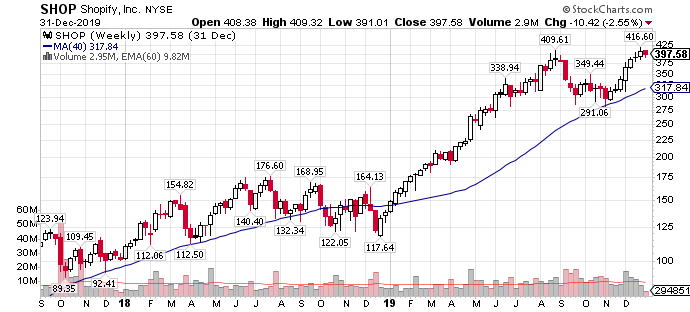

Shopify is the stock I have completely missed to this point as I have never owned a share. It happens, sometimes you miss and continue to hesitate to get in. One may argue, “why now” at nearly $400 per share. The stock is extended so I wouldn’t advise to buy at the moment but it’s one I advise to watch for the proper setup or pullback as this company is a beast. It might have a large correction coming, to digest prior gains and 2020 may not be its year but I can no longer ignore.

Sales have increased from $222.8MM to $390.6MM the past eight quarters, averaging gains of 57% QoQ. Minus last quarter, earnings have turned positive the past two years and expect to jump considerably in 2020. Institutional sponsorship has jumped 70% the past two years, with more than 1,000 funds currently holding shares.

I am not buying at the moment but watching for an ideal setup with better risk-to-reward.

-

SE – $40.22: Sea Limited engages in the digital entertainment, e-commerce, and digital financial service businesses in Taiwan, Thailand, Vietnam, Indonesia, and internationally. It provides Garena digital entertainment platform for users to access mobile and PC online games, and eSports operations; and access to other entertainment content, such as live streaming of online gameplay and social features.

What stands out most about SE is the accelerating sales figures, increasing from $124.6MM in December 2017 to $610.1MM in September 2019, a near 500% increase in two short years. The QoQ numbers are averaging gains of 112% the past eight quarters with figures increasing every quarter – amazing. The downside, earnings are negative and look to stay this way for at least another year.

The stock is based in Singapore so institutions have been shy in accumulating shares, with only 276 funds reporting in the latest period. Shares have increased by more than 200% the past twelve months with a big gap-up in November. I prefer gaps to close before moving higher so we’ll see how SE reacts going forward. Shares are currently extended so I am not buying right now. I like the growth story and future potential so I will watch until an ideal setup presents itself.

I do not own shares and will wait for a proper setup.

Tickers included:

STNE, OKTA, ROKU, ZM, LVGO, WORK, SQ, CGC, CRWD, TCEHY, PYPL, MDB, SNAP, SHOP, SE

Previous Stocks to Watch Lists:

January 1, 2019: Stocks to Watch 2019

January 1, 2018: Stock Trends for 2018

Chris,

Are this stocks at current valuations are safe to enter fresh?

Visionary (at least for the most part)!

This was an amazing read.

Almost all of your picks have been thriving

Great post and I hope you do this every year. I’m in a similar demographic to yourself, age and employment-wise, so it’s great to get insights from someone who has been doing this much longer than myself. It would be interesting to see where a lot of these would have been without the pandemic – still very successful but Shopify…? Wow.

Will stay tuned in January for some inspiration but if you don’t mind me asking, how do you track these and curate these lists? Reading this it sounds as though you’ve previously held some or art least held some these alrteady for a while. What other processes do you go through to identify your shortlistees if you don’t mind me asking?

Thanks in advance.

Amazing! Thats all I can say.Comparing to where they are now.

Hi Chris

Lovely to read your post – you are a true inspiration for a beginner on the dangerous markets.

Can you tell me when you are going to make a list with stocks to watch for 2021?

I am looking forward to this!

Best regards – Mathias from Denmark