“Stand by your stocks as long as the fundamental story of the company hasn’t changed”

– Peter Lynch

This is what the Stocks to Watch 2021 list is going to consist of. I’m standing by the stocks and brands that I trust the most. I own several of these stocks already and plan to hold them while looking to add others. While the products and services of these stocks are well known and are not going anywhere anytime soon, their stock prices will fluctuate. This is NOT a buy list, it’s a trends list containing stocks of companies I believe will be around for years, growing sales and earnings, regardless of their recent performance.

I am sticking with the steady and consistent performers this year, stocks and companies that have proven themselves already. I have sprinkled in a few newbies but the bulk of the list are known brands. I believe this will be the trend going forward while smaller and lesser-known stocks will be volatile with short-lived hype.

I’m not posting the latest fad list of growth stocks that may pump up quickly in the matter of weeks or months only to worry if they will they collapse. Let’s leave that to the traders because I trade poorly.

Boring? Perhaps, but that’s great investing as the big trends last for years.

We should NOT want to be in-and-out of positions quickly. We should want to hold them, over time. We want to learn to be patient during drawdowns and negative headlines, knowing the story of the underlying stock has not changed. This is a lot easier said than done, especially in today’s world of instant satisfaction and gratification.

Playing the long game is a lesson that has been flashed to me constantly over the past twenty years but I think I am only starting to learn it now. I hope to continuously get better at applying this lesson over the next twenty years as it will substantially increase my bottom line.

2020 was an incredible year, in terms of the stock market and particularly growth stocks. The Stocks to Watch 2020 list finished the year with a collective gain of 202.35%, an incredible feat during a global pandemic. It was not surprising as many of the trends I identified in January were only accelerated by the pandemic, QE and the work-from-home lockdowns. All 15 stocks showed a gain and 12 of the 15 ended with a triple digit gain. LVGO was the biggest gainer, up 457.74%.

I don’t expect 2021 to repeat this feat so our expectations need to be set now, back to historical norms. In fact, I see several of these stocks as extended and beyond ideal entry areas and know they may be vulnerable as I post this annual list on an arbitrary date every New Year. Please pay attention to the individual analysis as several of these stocks are ripe for a deeper correction which will allow for better setups in the future. If you own them already, hold patiently and look to add on constructive dips.

Nothing on this blog is a recommendation to buy, sell or hold, rather it’s a diary of my own analysis into yearly trends. Again, this is NOT a buy list. This list identifies trends which I believe will continue to last for years.

I screen, watch and then buy stocks based on a few simple parameters:

- Great product, service and brand

- Rising sales QoQ and YoY

- Rising EPS QoQ and YoY or EPS looking to turn positive (from negative territory)

- Increasing institutional sponsorship

- Technically: grabbing near support, at a breakout or within a base (near the 50d or 200d moving average)

That’s really it – I keep it simple.

I must repeat what I said last year and will repeat every year:

The annual “Stocks to Watch” list often includes newer and up-coming growth stocks that I own or candidates I am looking to own. Stocks such as AAPL, AMZN, GOOGL, MSFT, NFLX, FB, V, MA, etc. should be owned in almost every portfolio already, whether in your active trading account or a more passive retirement account. Own those stocks as they will all likely double or triple over time, once again. Own an index fund as well and add dollars to it annually, during up and down years – just do it and check back in 30 years.

Honestly, 95% of all folks should just own index funds and call it a day and forget about trading or investing in individual equities.

My annual blog post, Stocks to Watch, targets equities that I trade within my active investing account, an account that’s smaller and more active than my conservative accounts (retirement, index and company stock). I don’t disclose the number of shares or the size of the account as that’s personal information. What I will disclose, here and on twitter, is what I own, what I buy and what I sell. I do believe in being transparent with the equities I hold as well as the equities I don’t when discussing them on the blog or social media.

I don’t trade for a living nor do I aspire to trade for a living. I invest to increase my overall net worth and to “play the game”. I do get a thrill at trying to beat the market averages by making my own decisions. Some years this works and in others, it doesn’t.

“Know what you own, and know why you own it” – Peter Lynch

Let’s dive into the trends and my favorite brands to own in 2021:

Trends that will continue during and post COVID & 30 stocks I like across the groups:

- E-commerce: SHOP SE PINS ETSY CHWY

- Payments: SQ PYPL

- Security: CRWD OKTA ZS

- Edge & Cloud: FSLY NET APPS TWLO

- Database: MDB DDOG PLTR

- Health: TDOC GDRX

- Fitness: PTON

- Streaming: SPOT

- Digital Adv: ROKU TTD

- Tech Utilities: ZM DOCU CRM U FVRR

- Services: UBER ABNB

NOTE: The bottom of this blog post lists 10 additional stocks that I considered but didn’t make the official cut (mostly newer names) and the 17 growth stocks I own as of today.

Enjoy my 15 Stocks to Watch for 2021, in no special order (stocks I own on this list = *):

TDOC*, PINS*, CRWD*, FSLY*, NET, APPS, DDOG*, U, PTON, ROKU*, ZM*, DOCU, CRM, UBER*, ABNB

-

TDOC – $199.96: Teladoc Health, Inc. provides on-demand virtual healthcare services on a business-to-business basis with over 3,000 board certified physicians globally. The company merged with Livongo last year, which was one of my top plays and best performing investments.

Sales have been increasing the past several quarters with an average QoQ gain of 53% for the most recent eight quarters from $122.7MM to $288.8MM for a total gain of 135%. Institutional sponsorship is up 88% from 651 funds to 1,230 funds the past four quarters.

Technically, the 50d moving average and 200d moving average are converging in a six-month sideways pattern. The stock is currently sitting in an ideal accumulation zone. I recently added more shares and currently hold a position. It’s one of my strongest conviction stocks in the years ahead.

I am long shares of TDOC

-

PINS – $65.90: Pinterest, Inc. provides a visual discovery engine globally allowing people to find inspiration for their lives, including recipes, home and style ideas, travel destinations and others. Revenues are expected to reach more than $1.5 billion in FY 2020.

Sales were disrupted briefly during COVID but have bounced back and have maintained a QoQ gain of 46% the past eight quarters from $273.2MM to $442.6MM for a total gain of 169%. Institutional sponsorship is up 76% from 515 funds to 907 funds the past four quarters.

The stock has run from a low of $10.10 in March to a high of $72.88 in December. It’s extended from the 200d ma but riding the 50d ma. I bought PINS in July at $24.57 so it’s easy for me to say “stay put”. With that said, I feel PINS has room to continue this run based on the institutional accumulation. However, I would allow it to form a fresh base before looking to open a new position.

I am long shares of PINS

-

CRWD – $211.82: CrowdStrike Holdings, Inc. provides cloud-delivered security solutions for next-generation endpoint protection in the United States and internationally. The Falcon platform runs through a software as a service subscription-based model that covers various security markets, such as endpoint security, security and IT operations, and threat intelligence to deliver comprehensive breach protection against sophisticated attacks.

Sales have averaged a QoQ gain of 92% the past eight quarters from $80.5MM to $232.5MM for a total gain of 189%. Institutional sponsorship is up 364% from 203 funds to 942 funds the past four quarters. Funds can’t get enough of CRWD recently and I love owning what the funds own.

I bought CRWD on February 25, 2020 at $56.75, just before the COVID market collapse. The shares plummeted to a low of $31.95 before rebounding and making a tremendous run to a high of $227 in December. I held during the March drop because I believed in the stock and still do today. Endpoint security protection is critical for today’s technology operations and I believe CRWD has a long runway, especially considering it’s a subscription based model.

With that said, the stock is extended and I wouldn’t recommend buying shares at these levels. Allow the stock to digest recent gains with a pullback and possible base formation at the 50d ma or even deeper at the 200d ma. Let’s keep an eye out for future base formations.

I am long shares of CRWD

-

FSLY – $87.37: Fastly, Inc. operates an edge cloud platform for processing, serving, and securing its customer’s applications. The edge cloud is a category of Infrastructure as a Service that enables developers to build, secure, and deliver digital experiences at the edge of the Internet.

Sales have averaged a QoQ gain of 42% the past eight quarters from $40.8MM to $70.6MM for a total gain of 73%. Institutional sponsorship is up 268% from 88 funds to 324 funds the past four quarters. Fund sponsorship is still relatively low and has a lot of upside potential if institutions want to get on board. The price will run if they get on board.

Technically, the stock has been trading in a six month range with resistance near the $100 threshold while support sits in the $70 range, an area where the 200d ma has now entered. I like the technology and industry so I am long shares.

I am long shares of FSLY

-

NET – $75.99: CloudFlare, Inc. operates a cloud platform that delivers a range of network services to businesses worldwide. The company provides an integrated cloud-based security solution to secure a range of combination of platforms, including public cloud, private cloud, on-premise, software-as-a-service applications, and Internet of Things (IoT) devices.

Sales have averaged a QoQ gain of 49% the past eight quarters from $55.5MM to $114.2MM for a total gain of 106%. Institutional sponsorship is up 186% from 138 funds to 396 funds the past four quarters. Sales are larger than FSLY and overall institutional sponsorship is higher but I think they can both do well going forward. I’m not smart enough to pick the winner so why not own them both.

I do not have a position in NET as of this writing as the price action got out ahead of me before I could grab. It’s currently 14% off of its all-time high and pulling back to the 50d ma for the first time since September. Some may see this area as an accumulation zone. I prefer the 200d ma to grab but that’s down near $44 right now. Let’s see how the stock reacts at the 50d ma. I’m looking to get in and will advise if and when I do.

-

APPS – $56.56: Digital Turbine, Inc., through its subsidiaries, provides media and mobile communication products and solutions for mobile operators, application advertisers, device original equipment manufacturers, and other third parties worldwide. Its software platform that enables mobile operators and OEMs to control, manage, and monetize devices.

Sales have averaged a QoQ gain of 52% the past eight quarters from $30.4MM to $70.9MM for a total gain of 133%. Institutional sponsorship is up 43% from 237 funds to 340 funds the past four quarters. I must note that sales the past two quarters has increased 93% and 116% vs the same quarters the prior year, the largest quarterly gains over the past two years. This is strength and explains why the stock doubled since October.

I missed this stock altogether in 2020 and then fumbled when it pulled back to $25 in October. I should have pulled the trigger but I didn’t (a mistake in hindsight).

Technically, this stock is extended from any ideal entry point. I will not chase which means I may continue to miss the stock, so be it. I will be watching to see if it constructively pulls back to the 50d ma and will advise if I grab shares at that time.

-

DDOG – $98.44: Datadog, Inc. provides monitoring and analytics platform for developers, information technology operations teams, and business users in the cloud globally. The company’s SaaS platform integrates and automates infrastructure monitoring, application performance monitoring, and log management to provide real-time observability of customers technology stack.

Sales have averaged a QoQ gain of 79% the past eight quarters from $61.6MM to $154.7MM for a total gain of 151%. Institutional sponsorship is up 313% from 164 funds to 678 funds the past four quarters. The quarterly sales growth has been amazing and funds on the street have been adding holdings into that sweet spot above 500 funds (this is where magic happens).

Technically, the stock has traded sideways for six months with a shorter three-month cup with deep handle base. The handle is deep but still acceptable and the pivot point remains at $111.59. I added more shares December 31st as I was completing my research for this post. It’s now an ~5% position for me.

I am long shares of DDOG

-

U – $153.47: Unity Software Inc. operates a real-time 3D development platform. Its platform provides software solutions to create, run, and monetize interactive, real-time 2D and 3D content for mobile phones, tablets, PCs, consoles, and augmented and virtual reality devices.

Sales have averaged a QoQ gain of 43% the past seven quarters from $116.5MM to $200.8MM for a total gain of 72%. Institutional sponsorship sits at 208 funds, the only quarter to report post IPO.

The stock IPO’d on September 18, 2020 and quickly blasted up from the $60 range to $120 by November and is now above $150, roughly 12% off of its all-time high of $174.94. The stock is trading in a range over the past five weeks between $140 and $170. Considering it’s a young stock, it’s difficult to establish any longer term support and resistance zones so if you like it, perhaps start a position. I will be watching to see how it reacts as the 50d ma closes in. I am interested in starting a position but being patient.

-

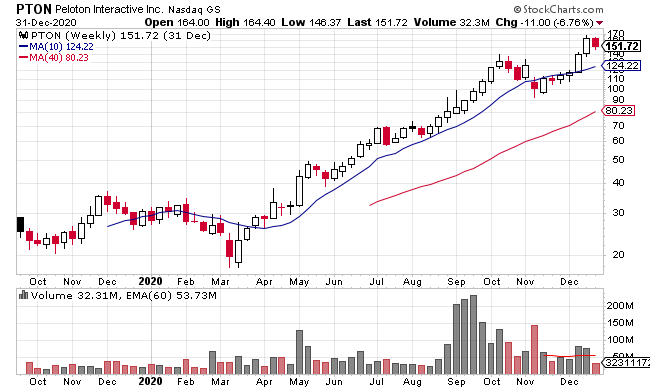

PTON – $151.72: Peloton Interactive, Inc. provides interactive fitness globally. It offers connected fitness products, such as the Peloton Bike and the Peloton Tread, which include touchscreen that streams live and on-demand classes. The company also provides connected fitness subscriptions for multiple household users, and access to all live and on-demand classes, as well as Peloton Digital app for connected fitness subscribers to provide access to its classes.

Sales have averaged a QoQ gain of 123% the past eight quarters from $262.9MM to $757.9MM for a total gain of 188%. Institutional sponsorship is up 236% from 195 funds to 657 funds the past four quarters.

If there’s one stock that I completely underestimated and got wrong in 2020, it was Peloton. I called it an expensive bike with an iPad strapped to it. Well, I couldn’t have been more wrong and have come around to admit that I didn’t understand the sub community and love for the interactive experience and brand. I own one now and have used it the past week and I quickly realized where I was wrong, in one short week. Hat tip to my wife as she convinced us to get one.

The stock has run from a March low of $17.70 to a recent high of $167.37 and can be classified as extended from an ideal entry area. PTON gave investors an opportunity to add shares in November when it pulled back to the 50d between $95 and $121. I would like to grab shares but will be patient and wait until it pulls back to the 50d ma. I also believe this stock can use a longer and deeper base before going higher. I believe it has potential over time and isn’t the fad I initially pegged it as. We’ll see.

-

ROKU – $332.02: Roku, Inc. provides a TV streaming platform and devices for entertainment.

Sales have averaged a QoQ gain of 53% the past eight quarters from $275.7MM to $451.7MM for a total gain of 64%. Institutional sponsorship is only up 14% from 759 funds to 871 funds the past four quarters but up 242% the past 8 quarters.

I stated that I missed this stock in 2019 but I didn’t in 2020. The position dropped nearly 30% after my buy but I held tight and it has worked out nicely, up from a low of $100.19 in June to a high of $363 in December. It was my conviction play of 2020 – believe in what you see and have patience during drawdowns.

The stock is roughly 8% from highs but is still extended from an ideal entry area, well above the 50d and 200d moving averages. Hold if you are in and let it settle if you would like to get in. This stock has a history of building multi month bases so be patient. Many are discussing FUBO on fintwit (I posted about it in December as well) but I still prefer ROKU and will keep my money parked here.

I am long shares of ROKU

-

ZM – $344.07: Zoom Video Communications, Inc. provides a video-first communications platform globally. The company’s product portfolio includes Zoom Meetings that offers HD video, voice, chat, and content sharing through mobile devices, desktops, laptops, telephones, and conference room systems.

Sales have averaged a QoQ gain of 170% the past eight quarters (top on this list) from $105.8MM to $777.2MM for a total gain of 635% (also top on this list). Institutional sponsorship is up 296% from 296 funds to 1,175 funds the past four quarters. The quarterly sales growth during COVID was amazing and expected, especially in hindsight. These growth figures will come back to earth and likely drop to double digits in the future, especially post COVID. With that said, I still like the company and its offerings beyond COVID (as much as I dislike the term, work has a “new normal”).

I recently grabbed shares as the right side of this three month base sets up down towards the 200d ma. I would not be surprised to see the stock trade below the 200d ma as the bottom of the base looks to establish itself. The ideal area to grab shares for a multiyear leader is near the 200d ma. I will look to increase the position once the base appears to have formed a bottom. A base like this can take months to a full year to play out, following the near 10x run (see the 2019 SQ base following it’s 10x run).

I am long shares of ZM

-

DOCU – $222.30: DocuSign, Inc. provides cloud based software, globally, using an e-signature solution that enables businesses to digitally prepare, execute, and act on agreements.

Sales have averaged a QoQ gain of 41% the past eight quarters from $199.7MM to $382.9MM for a total gain of 92%. Institutional sponsorship is up 74% from 762 funds to 1,332 funds the past four quarters.

The stock made an amazing run from the $50 area in the summer of 2019 to a high of $290.23 in August 2020. The high was briefly visited during what appears to be a slightly rising sideways six month base as price rides along the 50d ma. The 200d ma has closed considerable ground vs price since they touched back in March.

One may consider to add along the 50d ma or wait to see if the 200d ma closes the gap at which time would make an ideal risk/reward setup. I think DOCU has more room to run and will be watching to see if it gets closer to the rising 200d ma (remember, so many thought TDOC would not touch the 200d and we’re there now). They all eventually come back to the 200d.

-

CRM – $222.53: salesforce.com, inc. develops enterprise cloud computing solutions with a focus on customer relationship management worldwide.

Sales have averaged a QoQ gain of 27% the past eight quarters from $3,603.0MM to $5,419.0MM for a total gain of 50%. Institutional sponsorship is up 17% from 2,988 funds to 3,509 funds the past four quarters.

The stock is trading 22% off of all-time highs, set in September, and is now trading back towards the 200d ma. Historically, CRM has been an ideal buy every time it trades back towards the 200d ma so that’s why I am interested. I was a fan of Slack (WORK) before CRM acquired it and believe it can help in their suite of offerings but by no means is that the reason why I am interested (just an added benefit).

I plan to allow the stock to smooth out this four month base and catch support at or near the 200d ma before considering a buy (it’s getting close).

-

UBER – $51.18: Uber Technologies, Inc. develops and operates proprietary technology applications globally. It connects consumers with independent providers of ride services for ridesharing services, as well as connect consumers with restaurants and food delivery service providers for meal preparation and delivery services.

Prior to COVID, sales averaged a QoQ gain of 25% between Dec-18 and Dec-19 from $2,974.0MM to $4,069.0MM for a total gain of 37%.

Post COVID, sales have dropped to an average QoQ gain of only 11% the past eight quarters from $2,974.0MM to $3,129.0MM for a total gain of 5%.

Institutional sponsorship is up 37% from 894 funds to 1,226 funds the past four quarters.

In my opinion and as an investor in UBER (bought shares July 17, 2020 at $32.46), folks should focus on pre-COVID sales growth, recent sales growth as we navigate through COVID and future post-COVID sales growth. The stock is up 57% since my purchase, which is based on the future of this company and their “verb-like” status in society: “Call an Uber”.

The price has been moving sideways over the past six weeks after the 50% run from the gap-up in November. An ideal grab can happen near the 50d ma or support above $48.

I am long shares of UBER

-

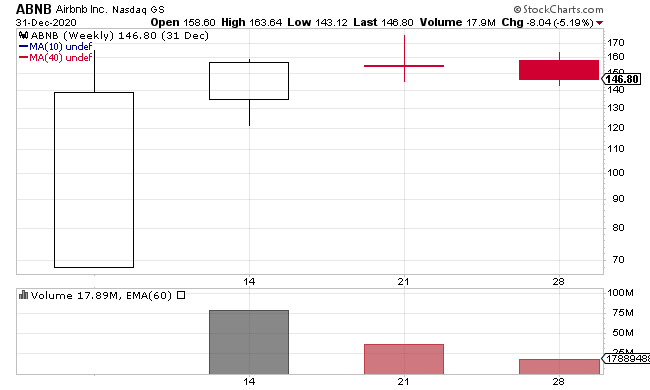

ABNB – $146.82: Airbnb, Inc. operates a platform for stays and experiences to guests worldwide. The company’s marketplace model connects hosts and guests online or through mobile devices to book spaces and experiences.

Prior to COVID, sales averaged a QoQ gain of 32% between Dec-18 and Dec-19 from $840.6MM to $1,106.8MM for a total gain of 32%.

Post COVID, sales have dropped to an average QoQ gain of only 9% the past eight quarters from $840.6MM to $1,342.3MM for a total gain of 60%.

Institutional sponsorship has not been reported yet due to the recent IPO on December 10, 2020.

Similar to UBER, I hold the same opinion that folks should focus on pre-COVID sales growth, recent sales growth as we navigate through COVID and future post-COVID sales growth. The stock looks expensive near $146 but is already 16% off highs. It’s too early to identify a base or use major moving averages so it’s a purely discretionary decision right now, using fundamentals and brand.

Figures aside, I have had great experiences using Airbnb in multiple locations and feel others have had the same. I believe the company will continue to grow and expand offerings post COVID so it’s one to watch.

I don’t own shares today but I am interested due to the simple fact that it’s a strong brand and this is my theme heading into 2021. Strong brands.

I plan to screen for and watch other stocks in the market and won’t restrict myself to the 15 names on this list throughout the year. I have 30 names listed above and 10 additional below. I am excited for 2021 but cautious at the same time.

10 Additional Stocks I considered but didn’t officially make the cut – let’s track:

MWK, BIGC, NCNO, LMND, SKLZ, DKNG, AI, SNOW, ZI, BEPC

Growth stocks I own, a total of 17 positions as of 01/01/21:

CGC, CRWD, DDOG, FSLY, GRWG, MDB, OKTA, PINS, PLTR, ROKU, SE, SQ, TCEHY, TDOC, TTD, UBER, & ZM

The plan throughout 2021 is to hold and/or rotate the portfolio into my strongest conviction stocks = best brands.

Previous Stocks to Watch Lists:

January 5, 2020: Stocks to Watch 2020

January 1, 2019: Stocks to Watch 2019

January 1, 2018: Stock Trends for 2018

Thanks for your reasoning of your conviction list. I also just read the initial post Great success secrets and stock screeners and few others. Your sharing and giving back to Fintwit and trader community is appreciated. Happy new year , hope you and your family prosper with health and wealth in new year.

Amazing work you have done again. I own a lot of those stocks as well. Its a pleasure to read about it from your perspective. I can imagine you put a lot of work into it. I really appreciate it. Thanks a lot for that great work.