The analysis below will show you why I select this stock as the best bet when the builders eventually hit a bottom and start moving higher.

Nathan Rothschild, founder of one of Europe’s most-powerful economic dynasties, uttered one of the most frequently quoted maxims on investment timing in the early 19th Century when he said, “The best time to buy is when blood is running in the streets.”

Now, blood is running in the streets for this industry and the homebuilders are getting their rear-ends kicked by Wall Street, the media and anyone else that will jump on the bandwagon.

So, when will the bottom arrive? Who the hell knows? And if someone tells you they know, just walk away because they are fooling themselves and anyone who listens.

The bottom may be near but the upswing could take years if you go back and research history. Badly beaten down industries can take anywhere from two to five years to rebound and start trading higher.

With that said, I would like to tell you why I feel that NVR Homes (NVR) is the best bet when the bottom does arrive and we start to see some life in this area.

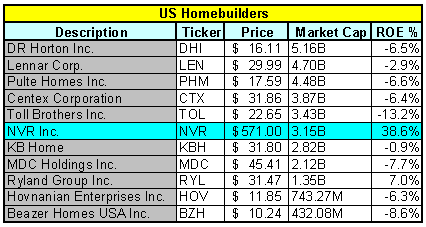

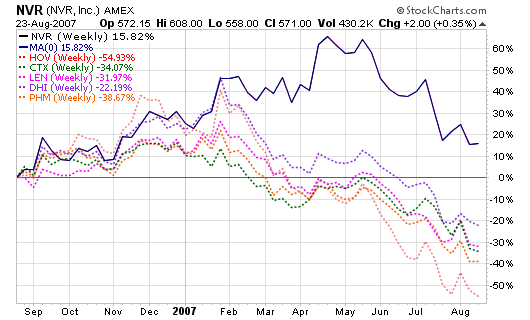

Let’s start with the charts above. They shows us that NVR now has the sixth largest market cap and is the only leading US Big Builder to boast a current ROE above the double digit threshold (positive of course). Of the ten other major players, only Ryland Group (RYL) has a positive ROE while writing this piece. This is major because every one of these stocks were reporting 20%+ ROE’s over the past five to seven years with several of them averaging 35% or better. NVR had an ROE of 105.2% in 2003, 78.7% in 2004 and 92.3% in 2005.

NVR was one of the smarter builders by scaling back their land purchases in 2005 and 2006 when everyone else was going nuts buying land that was way overvalued. They were also the only homebuilder to receive a report card grade of A- by Big Builder Magazine in the May 8, 2007 edition. The magazine said:

NVR’s inimitable focus on EPS growth through capital allocation discipline and land-risk minimization has positioned the company to weather a deep and long downturn in superb condition. The company’s extreme concentration in the Washington, D.C., market and its immediate environs exposes it to that market’s vulnerabilities but allows for peerless operational discipline and flexibility in light of situational opportunities that emerge before a wider recovery. The company’s market share strength in its competitive arena give it leverage in renegotiating terms on optioned takedowns, allowing the builder to remain in control of assets even in a slower sales pace environment.

Connect with Me