The builder’s index was up more than 10% this week (July 20-24, 2009), one of the leading groups in the market. The industry is still badly beaten and I do not own shares in any of the companies listed and I don’t plan to buy any time soon. Like I said two years ago in the blog post The Best Home Builder Stock

“The bottom may be near but the upswing could take years if you go back and research history. Badly beaten down industries can take anywhere from two to five years to rebound and start trading higher.”

Give it time, past industries can and usually do take years to recover. The one “prediction” I did make has held true, NVR continues to be the group’s leader. Since my blog post on 8/24/07, NVR is the ONLY stock showing a gain with Hovnanian still down more than 75%. Toll Brothers is a distant second with a 10.77% loss.

(NVR) NVR Inc.: + 7.74%

(TOL) Toll Brothers Inc.: -10.77%

(MDC) MDC Holdings Inc.: -19.99%

(DHI) DR Horton Inc.: -22.76%

(RYL) Ryland Group Inc.: -30.15%

(PHM) Pulte Homes Inc.: -40.29%

(KBH) KB Home: -43.33%

(LEN) Lennar Corp.: -58.49%

(CTX) Centex Corporation: -67.11%

(BZH) Beazer Homes USA Inc.: -75.27%

(HOV) Hovnanian Enterprises Inc.: -75.99%

I guess it helped to work in this industry during the boom for approximately five years but I am sill surprised that some of the big guys haven’t merged or taken over their competitors.

Other than Housing, Biotech and Cyclicals also lead the market this past week (+26% & +10% respectively), these are not the groups of choice for leaders (in my opinion).

Here’s the original post from August 24, 2007:

The analysis below will show you why I select this stock as the best bet when the builders eventually hit a bottom and start moving higher.

Nathan Rothschild, founder of one of Europe’s most-powerful economic dynasties, uttered one of the most frequently quoted maxims on investment timing in the early 19th Century when he said, “The best time to buy is when blood is running in the streets.”

Now, blood is running in the streets for this industry and the homebuilders are getting their rear-ends kicked by Wall Street, the media and anyone else that will jump on the bandwagon.

So, when will the bottom arrive? Who the hell knows? And if someone tells you they know, just walk away because they are fooling themselves and anyone who listens.

The bottom may be near but the upswing could take years if you go back and research history. Badly beaten down industries can take anywhere from two to five years to rebound and start trading higher.

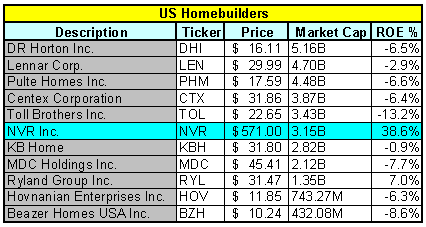

With that said, I would like to tell you why I feel that NVR Homes (NVR) is the best bet when the bottom does arrive and we start to see some life in this area.

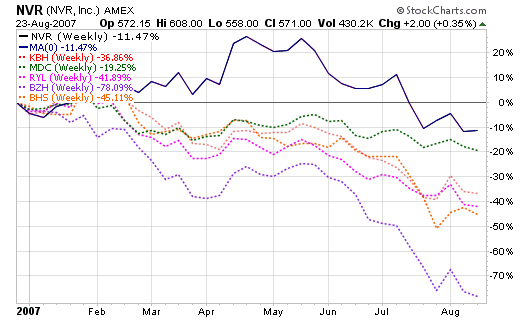

Let’s start with the charts above. They shows us that NVR now has the sixth largest market cap and is the only leading US Big Builder to boast a current ROE above the double digit threshold (positive of course). Of the ten other major players, only Ryland Group (RYL) has a positive ROE while writing this piece. This is major because every one of these stocks were reporting 20%+ ROE’s over the past five to seven years with several of them averaging 35% or better. NVR had an ROE of 105.2% in 2003, 78.7% in 2004 and 92.3% in 2005.

NVR was one of the smarter builders by scaling back their land purchases in 2005 and 2006 when everyone else was going nuts buying land that was way overvalued. They were also the only homebuilder to receive a report card grade of A- by Big Builder Magazine in the May 8, 2007 edition. The magazine said:

NVR’s inimitable focus on EPS growth through capital allocation discipline and land-risk minimization has positioned the company to weather a deep and long downturn in superb condition. The company’s extreme concentration in the Washington, D.C., market and its immediate environs exposes it to that market’s vulnerabilities but allows for peerless operational discipline and flexibility in light of situational opportunities that emerge before a wider recovery. The company’s market share strength in its competitive arena give it leverage in renegotiating terms on optioned takedowns, allowing the builder to remain in control of assets even in a slower sales pace environment.

Financially, the company is maintaining its leadership role in areas such as cash flow, earnings, long term debt, ROA, ROE, net income and revenue. Since they are writing off the least amount of land due to their foresight in 2005, they are managing to keep their financial numbers above their peers and remain the best investment from this industry for Wall Street.

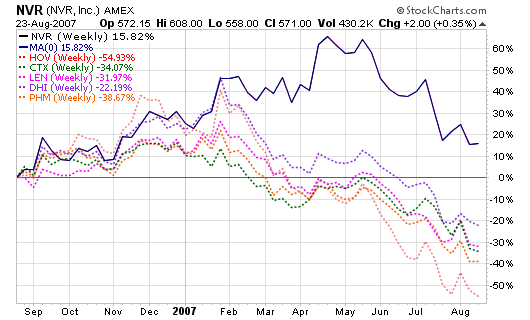

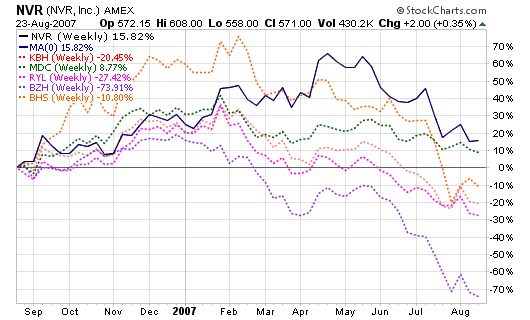

Finally, we must look to the charts where we see that NVR has the strongest relative strength (RS) rating versus every one of its peers in the industry. NVR is the only stock of the big builders to show a double digit gain over its price from one year ago; up 15.82%. Actually, MDC is the only other stock to show a positive gain from this time last year at 8.77%. Comparatively, BZH is down over 73% and HOV is down 55%.

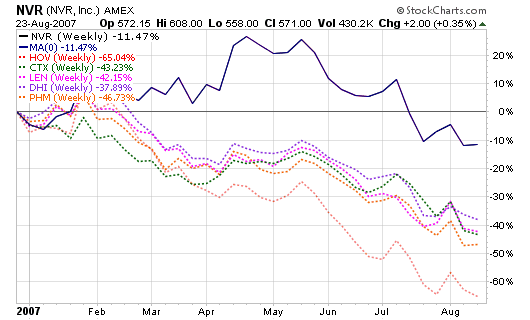

Looking at the next set of charts, we can see that NVR has dropped the least year-to-date versus the other leading builders in the US. They have only corrected by 11.47% while the rest of the pack has corrected by an average of 45%. Once again, BZH has dropped the most in 2007 at 78.09% with HOV right behind at 65.04%.

Therefore, I rate NVR the best value buy in this group when it decides to hit bottom and turn higher over the next couple of years. Long term, I see NVR reaching the $700 to $800 range while some of the other builders will still be struggling to reach $15 to $20 per share. Amateur investors may argue that it is easer for a $12 stock to go to $20 but I will argue and place my money behind the $550 stock to move $250 points higher to $800. NVR almost reached $1,000 per share at its peak and I have no doubt that we will see it there one day but that could take a long time and beaten down industries need years to recover.

FYI: I do NOT own any shares in any of the companies listed below. If I do buy in this industry, it will most likely be NVR based on the intelligence of its management leadership.

Closing prices from 8/23/07:

(DHI) DR Horton Inc., $16.11

(LEN) Lennar Corp., $29.99

(PHM) Pulte Homes Inc., $17.59

(CTX)Centex Corporation, $31.86

(TOL) Toll Brothers Inc., $22.65

(NVR) NVR Inc., $571.00

(KBH) KB Home, $31.80

(MDC) MDC Holdings Inc., $45.41

(RYL) Ryland Group Inc., $31.47

(HOV) Hovnanian Enterprises Inc., $11.85

(BZH) Beazer Homes USA Inc., $10.24

You must be dreaming… here’s the latest from Deutsche Bank there’s only one direction houseing’s going and everything else with it.

NEW YORK (Reuters) – The percentage of U.S. homeowners who owe more than their house is worth will nearly double to 48 percent in 2011 from 26 percent at the end of March, portending another blow to the housing market, Deutsche Bank said on Wednesday.

Home price declines will have their biggest impact on prime “conforming” loans that meet underwriting and size guidelines of Fannie Mae and Freddie Mac, the bank said in a report. Prime conforming loans make up two-thirds of mortgages, and are typically less risky because of stringent requirements.

“We project the next phase of the housing decline will have a far greater impact on prime borrowers,” Deutsche analysts Karen Weaver and Ying Shen said in the report.

Of prime conforming loans, 41 percent will be “underwater” by the first quarter of 2011, up from 16 percent at the end of the first quarter 2009, it said. Forty-six percent of prime jumbo loans will be larger than their properties’ value, up from 29 percent, it said.

Of option adjustable-rate mortgages — which cut payments by allowing principal balances to rise — 89 percent will be underwater in 2011, up from 77 percent, the report said.

Chris,

Are you dense or dumb?…read my opening quote and the rest of the post for that matter: “The industry is still badly beaten and I do not own shares in any of the companies listed and I don’t plan to buy any time soon.”