I often get random questions from family members, friends, colleagues and social media followers that sound something like this: “I want to invest but I’m not sure what to buy, so can you recommend a few stocks.”

Or

I am saving for retirement (college fund, etc.), so where should I place my money (funds that they need to invest, commonly from an old 401k, a recent bonus, an inheritance, a stale IRA or whatever…).

They tell me that they trust my advice because I seem to know what I am doing. Perhaps it’s because I have a blog, twitter account or a Stocktwits following but I immediately reply by saying: well, be careful because I am not independently wealthy (yet), based solely on my market investments so take my advice with a grain of salt. I then go on to say: But if you are asking…

Index Funds!

What? INDEX FUNDS!

Says the guy who writes about stock investing and trading…?

I strongly suggest that the majority of people stay away from actively managed mutual funds, active investment managers, day trading, swing trading, trend trading, any trading, etc. I am not opposed to individuals buying and holding a handful of dividend paying blue chip stocks but why bother with the headache; go for the index fund and save your time for doing something fun.

Place at least 90% of your available investment cash “the serious money” into index funds and then actively speculate with no more than 10% of the rest. This 10% can be used to buy your speculative investments like $FB, $AAPL, $GOOG, $AMZN, $TSLA, $V, etc…

William Bernstein (author of The Four Pillars of Investing) once wrote:

“It’s bad enough that you have to take market risk. Only a fool takes on the additional risk of doing yet more damage by failing to diversify properly with his or her nest egg. Avoid the problem – buy a well-run index fund and own the whole market”.

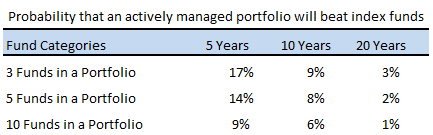

I agree: invest in one or more well-run index fund(s) that will promise a market return but with significantly lower fees. The average guy or gal in the 99% is not smart enough to “pick” the right stocks or mutual funds (or manager) at the right time. Heck, most fund managers in the 1% (Wall Street professionals) can’t do this either (data shows that greater than 80% of all fund managers fail to outperform the market over time).

Warren Buffett once noted that the moral of a story, as told in his 2005 Annual Report, is:

“For investors as a whole, returns decrease as motion increases.”

What does that mean? Well, let’s use a recent example of a bet Buffett made with a bunch of hedge fund managers back in 2007. The bet shows how an index fund mirroring the S&P 500 can outperform their actively managed funds, after fees, over a ten year period. They made a million dollar bet (winnings will be donated to charity) based on this premise and as of February 2016, eight years into the bet, Buffet is beating the all-star hedge fund managers 65% to 21%.

His Index Fund selection is crushing them and all he had to do was make a click or call to purchase the index fund and then he was done (not another minute was spent worrying about the investment). These managers (charging 2% on assets + 20% of performance) manage their funds daily and they are only 1/3rd of the return of Buffett’s choice (to date). So not only are they losing, they have spent eight years in their “professional job” losing to a fund that mimics the market.

Time = money so how do we even begin to quantify the hours spent by the hedge fund managers vs. the cumulative time that Buffett has saved doing other things. The extra time value is overwhelming so Buffett is much further ahead based on this ancillary bonus.

John Bogle (the founder of Vanguard) explains it this way in his book, The Little Book of Common Sense Investing:

“The way to wealth for those in the business is to persuade their clients, “Don’t just stand there. Do something”. But the way to wealth for their clients in the aggregate is to follow the opposite maxim: “Don’t do something. Just stand there.” For that is the only way to avoid playing the loser’s game of trying to beat the market.”

It means that the higher the level of investment activity, the greater the cost of investment fees and taxes, which ultimately results in a lesser net return for the investor.

I am an architect by degree so when I recall the famous quote by Ludwig Mies van der Rohe, “Less is More”, I suggest everyone apply it to investing as well.

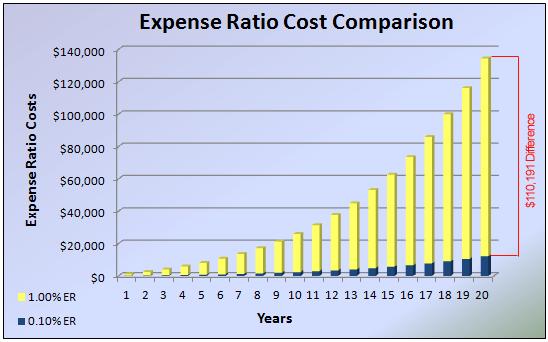

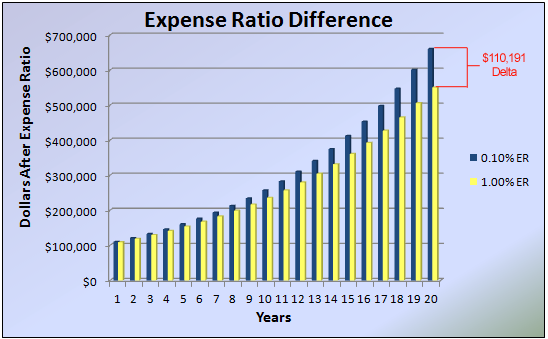

Less activity equals more return for the investor while more activity results in more profit for the fund managers leaving you, the retail client, with less retirement money in your pocket (see the charts and expense ratio matrix below).

Charlie Munger stated:

“The general systems of money management [today] require people to pretend to do something they can’t do and like something they don’t. That is a funny business because on a net basis, the whole investment management business together gives no value added to all buyers combined. That’s the way it has to work. Mutual funds charge two percent per year and then brokers switch people between funds, costing another 3-4 percentage points. The poor guy in the general public is getting a terrible product from the professionals. I think it’s disgusting. It’s much better to be part of a system that delivers value to the people who buy the product.”

So based on what Buffett, Bernstein, Bogle and Munger have said…

Where do you now think the 99% should invest their money? What should YOU be doing with your money?

It’s obvious: Index Funds! At least 90% of your serious money, your retirement investments should be in low cost index funds. As you grow older, diversify to index bond funds as well.

Back in 1998, after opening my first investment account with Ameritrade, I would have thrown this advice in the garbage. If fact, I did. Who are Warren Buffett and these other old timers to say that I can’t trade and generate a return better than that of the market and my peers? The joke is on them.

Come on, my first trade (ever) in $AMD tripled; at 20 years of age (while taking 18 architecture credits that semester). I’m the next “Master of the Universe” but I am going to do it from my computer, not slaving 80-100 hours per week wearing a suit and working for a firm like Goldman Sachs. Not that Goldman would take me but you get the point.

Well, the 2000-2001 market taught me! All that (dot-com) money from 1998-2000: gone. Even after that losing experience, I had to find the Holy Grail and learn how to outperform the market. I spent the next decade or so in search of the answer. I made some money and I lost some money but the most important lesson was what I learned about myself (trading is often a reflection of yourself, your emotions, your beliefs, etc.). I also finally learned that the market is rigged, rigged against the common guy with fees, commissions, taxes, marketing schemes, front running, etc. You name it and it’s being done. Can “dumb money” (retail investors) beat Wall Street’s “smart money”, the professionals?

“By periodically investing in an index fund, the know-nothing investor can actually outperform most investment professionals. Paradoxically, when ‘dumb’ money acknowledges its limitations, it ceases to be dumb…. Those index funds that are very low cost… are investor-friendly by definition and are the best selection for the most of those who wish to own equities.” – Warren Buffett

By investing in index funds, your “dumb money” ceases to be dumb. And your hard earned cash is no longer lining the pockets of Wall Street professionals who essentially are running a marketing business, not an investing business looking out for the best interest of their retail clients.

Fast forward to 2016, a solid 18 years later and I’m hopefully a bit wiser based on the fact that I wholeheartedly agree with the old timers. The advice I now give to family, friends, colleagues and my children is: INDEX FUNDS, then go do something else with your time (exercise, play sports, travel, start a business, write or anything that makes you happy). Don’t waste your time trading.

I love the market. I love researching stocks, viewing charts, writing on this blog and throwing my thoughts onto social media but even I have noticed that I do less and less of it each year. Why, because of index funds. It’s easy, it’s quick and it wins. Mathematically, it can’t be debated. The “sales guys” and “marketers” on Wall Street will debate you and continue to sell you but don’t buy into their false pitch.

Does it help that I am not selling you anything? Perhaps. What I am selling you is a story, based on 18 years of experience of what works for the common investor, one that I am already starting to sell to my 7 year old. I prefer he start a business, several businesses for that matter, rather than get wrapped up in trading stocks.

A few trades in my investing life have taught me to truly follow the idea that:

“The real money in investment will be made not out of buying and selling but of owning and holding securities.” – Benjamin Graham

I have lost more money, not by buying incorrectly but by selling (far too early). If I would have held some of my early trades in $GOOG, $AAPL and others, I would be a far richer individual today. But I needed the action and wanted to scalp the quick profit – well, the quick action cost me big time over the long run. In every instance, I would have been better off today, if I held through to TODAY.

So, to anyone on social media reading this, go setup up an automatic withdrawal that gets distributed into your Index Fund account each month and let it ride, until retirement! Don’t touch it but keep adding on a consistent basis and you will outperform 99% of your peers and at least 80% of the professionals.

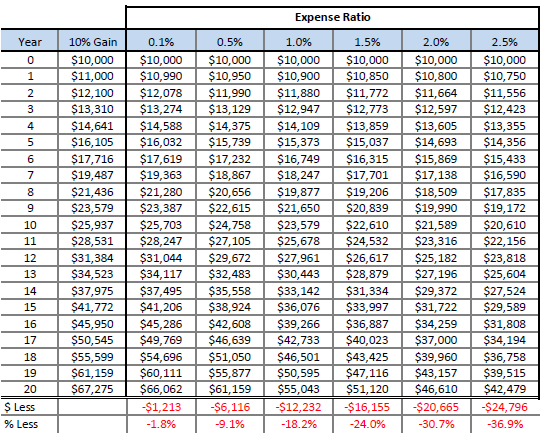

NOTE: Vanguard has index funds that have expense ratios of .1% and less. I own one in my 401K that is at .04%. Look at the difference between .1% and 1%, 2% and more. Now multiply this by hundreds of thousands in the account and it becomes absurd, the amount of fees that Wall Street keeps to themselves to underperform. A factor of 10, takes the $12,232 in the 1% ER column and puts it at more than $122,000 of your money, in their pockets.

NOTE: S&P 500 ($SPY), Total Returns since 2009 (market bottom).

- 2009: +26.4%

- 2010: +15.1%

- 2011: +1.9%

- 2012: +16.0%

- 2013: +32.2%

- 2014: +13.5%

- 2015: +1.2%

- 2016 YTD: +2.0%

We’re likely due for a negative year or two… Will the Index Funds drop less than actively managed funds, after fees? If dollar cost averaging (throughout), data shows that Index Funds won during the 2008 down turn, the 2000-01 down turn, etc. They win over time combined with low fees and minimal activity.

Chris,

Around paragraph 9 you state, ” I agree: invest in one or more well-run index fund(s) that will promise a market return but with significantly lower fees.”

Can you list what you consider to be well-run index funds that WILL PROMISE a market return?

Thank you in advance for a reply to this question.

MP Sunday

The problem with index funds is that almost all of them are market-cap weighted. Despite that, I have a couple, but they don’t have more than about 100 stocks in them. I also have some blue-chip stocks that have had growing dividends for many years.

Only recently have other index funds appeared that are (more or less) equal weighted. Those I’m very interested in, though my asset allocation to stocks is sufficient for now.

Great advice! I also learned the hard way that by trading more you end up losing more. I now buy index ETFs and hold them for good. Also, because I’m not selling them I’m not hit by 23.8% long term or almost 40% in short term taxes. Nothing will beat that once you factor taxes and commissions. I do a couple more things to ‘spice it’ up, but that’s not for the regular joe investor out there.