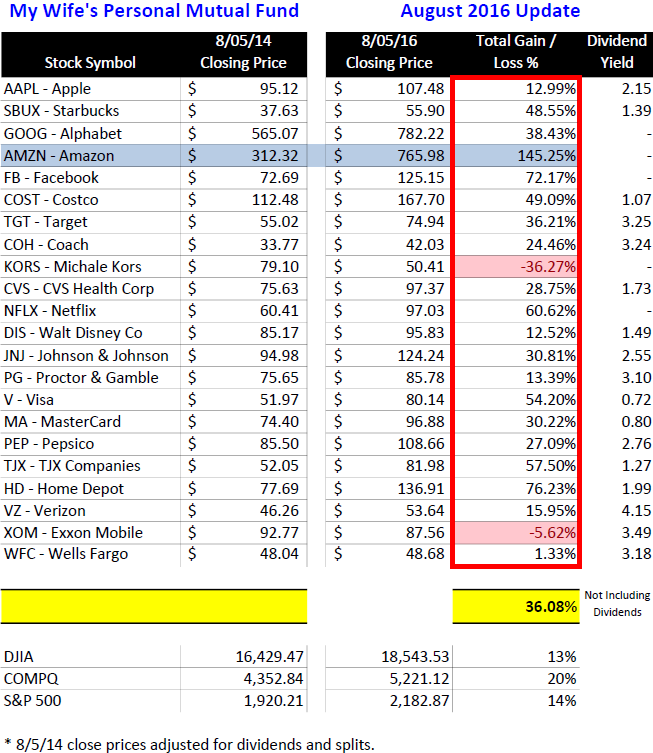

Back in August 2014, I decided to put a collection of stocks together that represent the products and services of companies used most often by my wife and family. I decided to call it “My Wife’s Mutual Fund”.

Original Post:

August 6, 2014: My Wife’s Personal Mutual Fund Outperforms the ProsFollow-ups:

February 21, 2016: My Wife’s Personal Mutual Fund Crushes the Markets, AGAINAugust 7, 2016: My Wife’s Buy & Hold Strategy Still Crushing the Professionals

Based on past experience, I noticed that these companies were outperforming the market by a wide margin, especially on an individual basis.

What started as a playful review, became a serious pursuit of stocks that we decided to grab shares in. We don’t own every stock on the list below but we do own and have owned many over the years.

As of November 19, 2017, the 22 stocks have performed as follows (for purposes of the exercise, no trades have been made):

- Total gain of 66.87% (adjusted for dividends & splits)

- 19 of the 22 stocks show a gain

- 17 of the 22 stocks show a double digit gain

- 11 of the 22 stocks show a gain of at least 50%

- 6 of the 22 stocks show a gain greater than 100%

- The leading gainer, also the 2nd highest initial priced stock, is up 264%: Amazon $AMZN

- 3 stocks show a loss: $CVS, $XOM and $KORS

- An 86% success ratio

I’m not surprised to see, after years and years of gains (pre-2014), that these stocks continue to outperform the general market indexes. At this point in 2017, I believe that many of these stocks will continue to outperform in the years to come (and I’m making this statement deep into a multi-year up-trend).

I subscribe to a strategy of “keep it simple”. The run from March 2009 has certainly helped but these types of companies should continue to outperform going forward (a few may fall out of favor but the stronger ones will continue to dominate and innovative within their respective categories).

Connect with Me