The trends that I am watching in 2017 are not much different than what I have been following and investing in over the past two years. As Newton’s first law stated,

“An object in motion continues in motion…”.

I could search for the “next hot thing”each year but why make investing more difficult than it already is when certain trends, technologies, products, services and companies continuously work.

Perhaps this list is old and boring (Buffett likes boring) but we’re here to make money, not be sexy.

Investing in the stock market should not be exciting or a path to get rich quick, rather it’s meant to moderately grow our existing capital over longer periods of time.

As I grow older, I have learned that I can beat most investors by being average. By investing (longer term) in low cost index funds and an assortment of stocks that have proven their worth, my returns have consistently outperformed social media stock pickers, active managers and mutual funds.

In fact, I suggest that 99% of all investors stick with low cost index funds and skip individual stocks altogether.

Ask yourself: why would you risk your capital with an active manager who will likely underperform over time, once the fees and activity eat away at the gains?

The S&P has provided an annualized gain of 14.5% over the past 8 years while the Nasdaq 100 has provided a 20.4% annualized gain. That’s a cumulative gain of 195% and 339% respectively.

I haven’t seen many active managers do better than this over the same period. Once again, why risk the guess work of tops, bottoms, trends, fees, commissions, etc.? If active managers were performing 2x-3x+ the averages, over 10+ year periods, then I would consider their services.

Now, let’s get to the list (which contains much of the products and services I use, as well as several of the stocks I already own):

*NOTE: the overall health of the markets must be positive for many these investments to do well.

Digital Currency:

As I did in 2015 (Stock Trends for 2015), I will skip the details surrounding blockchain and Bitcoin (which is above $1,000 as this post). Cash is still king worldwide, as more than 80% of all transactions globally (and 40% in the United States) are still carried out using cash, particularly transactions involving small amounts of money. So why is this good? Because the growth opportunity of electronic transactions is still substantial. I own several on the list and would recommend any of the seven.

- PYPL: $39.47. PayPal operates as a technology platform company that enables digital and mobile payments on behalf of consumers and merchants worldwide. The stock appears to be building a solid base above the up-trending 200d ma. A few more solid earnings reports and I can see the stock making a 50% move in 2017, from $40 to $60, riding that 200d ma higher.

- AMZN: $749.87. Amazon Payments service competes with PayPal, Apple Pay, and Google Wallet, already owns a sizeable market share and may be its most “underappreciated” business, per RBC Capital. The stock is consolidating near it’s 200d ma and if it holds, could be poised for the next leg higher ($750 to $1,000?).

- V: 78.02. Visa operates the world’s largest retail electronic payments network and is one of the most recognized global financial services brands. The stock has been mostly sideways over the past 6-12 months and is currently below the 200d ma during a multi-year up-trend. As a long-term shareholder, I’m holding, until it proves otherwise.

- MA: 103.25. MasterCard operates the world’s second largest retail electronic payments network. Like Visa, I will continue to ride and recommend this stock until it proves otherwise.

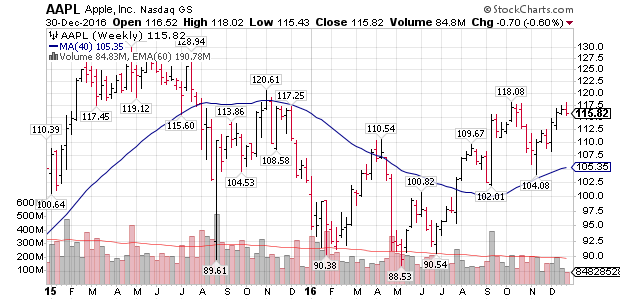

- AAPL: 115.82. Apple trailed its peers and the broader market in 2016 but may launch a comeback in 2017. The stock can be listed in several “trends” but I’ll place it here due to Apple Pay. The stock is back above its 50d and 200d ma’s. It needs a catalyst to make a run, perhaps the iPhone 8, a new technology and/or its electronic pay network? Deep down, I question whether the magic is gone, now that Jobs is long gone. We’ll see, but for now, I am still bullish on the company and stock. Adding shares below $100 has proved profitable over the past two years.

- GOOGL: 792.45. Alphabet has both Google Wallet and Android Pay (I am an Android guy, without a doubt). The stock is consolidating above the 200d ma and could be setting up for a run towards $1,000. With wallet, pay, advertising, self-driving cars, etc., the stock could be listed under most trends on this post.

- VNTV: 59.62. Vantiv is an electronic payment processing services to merchants and financial institutions in the United States. I placed the lesser known company/stock on my “13 Stocks for 2013 – 2nd Half” portfolio. I was early, as the stock traded mostly flat for the next 12 months but then it took off and more than doubled since. Like V and MA, it’s in a profitable business with excellent earnings. I can see this stock trading at $100 per share in the future.

Autonomous Driving:

Tesla, Ford, Uber, etc., each of these companies keep touting the revolution of self-driving cars. It’s coming and the technologies keep expanding. Nvidia was highlighted in 2015 and became the leader by going on a 440% tear, from $19.96 to a high of $119 in December 2016. The chips are hot again, therefore I added Intel to this list (another blast from the past).

- NVDA: 106.74. NVIDIA Corporation, operates as a visual computing company worldwide. The stock is up big over the past 6-12 months and may need some time to digest the gains. I would advise new investors to allow the stock to consolidate on lower volume above a support area, such as the 50d ma.

- MBLY: 38.12. Mobileye develops computer vision and machine learning, data analysis, and localization and mapping for advanced driver assistance systems and autonomous driving technologies. The stock is down since making my 2015 Trends list and has had a volatile ride with a high above $64 and a low of $23.57. Look for the stock to stabilize and mature a bit in 2017, now that the IPO is in the rear-view mirror. I could see a move from the upper $30’s to above $50 in 2017, however, it must recapture its major moving averages first.

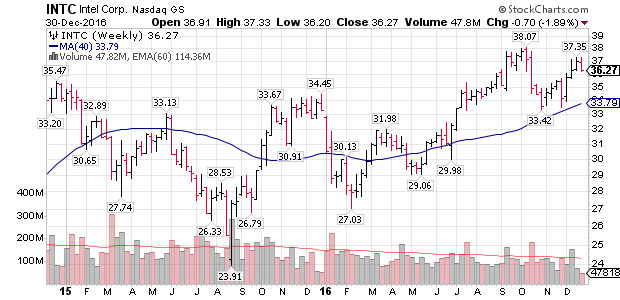

- INTC: 36.27. Intel designs, manufactures, and sells integrated digital technology platforms worldwide. Like NVDA, Intel is now in the self-driving game with its chips. The stock gained more than 20% from its low point of 2016 and is currently in an up-trend above the rising 200d ma. Chip stocks appear to be all the rage again (is this good or bad, as memories of the dot-com bubble appear in my head).

- TSLA: 213.69. Tesla Motors Inc. designs, develops, manufactures, and sells electric vehicles and stationary energy storage products. What can I say, I’m a big fan of Elon Musk. I added the stock due to the Musk factor but I am suspect. It’s struggling to recapture and sustain a move above its 200d ma. December was a big month for the stock but since 2015, it has been mostly flat with lots of volatility (similar to MBLY).

Technology / Internet Brands:

I am going with the technology/social media type stocks that we use most, Facebook and Netflix (AMZN, AAPL and GOOGL have already been listed). I don’t use BABA but they are the equivalent of Google in China (so going out on a limb here). I hate to admit this but I spend too much time on Facebook, Twitter and LinkedIn but on the flip side, I know millions of people do the same, which translates to advertising dollars. Social Media apparently triggers a dopamine high, which is alarming but from an investor’s standpoint, a jackpot. LinkedIn was acquired and TWTR’s stock is a mess so they will not be highlighted in 2017 (perhaps it’s the battle wounds of losing money several times on Twitter’s stock).

- FB: 115.05. Facebook operates as a mobile application and website that enables people to connect, share, discover, and communicate with each other on mobile devices and personal computers worldwide. More important is the data collection and advertising revenues. The stock has been struggling recently, from its high above $133, and must recapture its major moving averages. Short term, the stock looks volatile but long term, I am still bullish.

- NFLX: 123.80. Netflix is an Internet television network, engaging in the Internet delivery of television shows and movies on various Internet-connected screens. My family spends a lot more time on this platform than we do on cable or anything else (TV based). One can look to grab shares near or above an up-trending 200d ma.

- BABA: 87.81. Alibaba operates as an online and mobile commerce company in the People’s Republic of China and internationally. I view BABA as the Google of China, a market much larger than the US. Alibaba has entered artificial intelligence, the Internet of Things, connected cars, Fintech, big data, and more. The stock is showing a loss from my 2015 Trends list and has been volatile with a low of $57.20 and a high of $109.87. I anticipate the stock to stabilize as it matures, a couple years after its IPO. Google once traded below $100 per share – could this be the BABA opportunity, below $100? The government of China is the risk for BABA’s stock – unpredictable. Shares can be accumulated near an up-trending 200d ma (which is now).

- Others: already listed under previous trends: AMZN, AAPL, GOOGL

Cyber Security:

What do a billion Yahoo accounts, the US Department of Justice, countless retailers and the Election have in common? Hackers! The cyber security threat is only growing and it’s not going away. With mobile access, mobile banking, online banking, the connected home, cloud software, cloud servers, “cloud everything” and electronic payments, our wireless and digital world needs security protection. This trend was highlighted in 2015 and remains high on the list. The stocks within this group have had their runs and their fair share of volatility which has translated into average or below average returns. However, a few leaders should provide for good investments going forward. The four candidates below are the ones that catch my eye the most.

- HACK: 26.44. PureFunds ISE Cyber Security ETF seeks investment results that, before fees and expenses, correspond generally to the price and yield performance of the ISE Cyber Security Index. The ETF appears to be digesting the 2016 gains while it builds a base above the 200d ma. A buy above the 200d ma, in the mid-20’s, appears to be a nice risk/reward investment.

- MIME: 17.90. Mimecast Limited provides cloud security and risk management services for corporate information and email. The young stock had a nice run in 2016 and appears to be building the first base following its IPO. A buy near the 200d ma provides an ideal risk/reward entry.

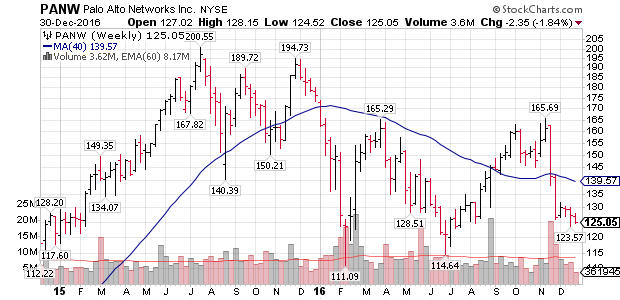

- PANW: 125.05. Palo Alto Networks provides security platform solutions to enterprises, service providers, and government entities worldwide. The rockstar stock from 2014-15 had its troubles in 2016 (falling from the summer 2015 peak of $200.55 to a low of $111.09 in February and $114.64 in June. It’s currently trading below its 200d ma which is not positive for an up-trend. Give it time to try and recover its major moving average, before any consideration to grab shares. I would not be surprised to see this stock trade above $200 in the future (when that day is – I have no idea, but we’re not sprinting here).

- CYBR: 45.50. Cyber-Ark develops, markets, and sells software-based IT security solutions that protect organizations from cyber-attacks. The stock just can’t seem to gain any momentum for a sustainable period of time. It’s been up and down for two years which has been frustrating as a prior share holder. The 200d ma appears to be heading north as the shares trade just below the major moving average. If it can recapture the 200d ma, one can test the investment by grabbing shares.

Others:

- BCS: 11.00. Barclays PLC, through its subsidiaries, provides various financial products and services worldwide. I bought the stock below $7 per share following the Brexit vote (shares fell more than 40% in two days). The trade was profitable so I locked in half my gains while holding the other half through to today. It’s not out of the question to buy back the shares I sold as a move towards the mid-teens is possible in 2017. Shares are a bit extended to start the year but any consolidation along the major moving averages will be a signal to add.

- USO: 11.71. United States Oil is an investment that seeks to reflect the performance, less expenses, of the spot price of West Texas Intermediate (WTI) light, sweet crude oil. It’s important for an investor to understand the investment they are making. The spot price of Crude Oil is different than buying USO (oil futures). With that clear, both USO and UWTI (before delisted) provided nice returns as investments in 2016. “Crude oil prices will recover modestly in 2017, thanks in part to the deal struck by most of the world’s oil producers” – Stratfor. Further, USO has an up-trending 200d ma with an eye on the mid-teens.

- XME: 30.41. SPDR S&P Metals and Mining ETF is an investment that seeks to provide investment results that, before fees and expenses, correspond generally to the total return performance of an index derived from the metals and mining segment of a U.S. total market composite index. With a Trump presidency confirmed, these stocks have been boosted since the election. They may digest some of those gains before moving higher again, throughout the year. I like a few individual stocks within the ETF (X, AKS, CLF) but I am not sure which ones will lead so going with the ETF is the safest route for now. One can grab shares on a consolidation near the 200d ma.

Some wisdom from Peter Lynch:

“The key to making money in stocks is not to get scared out of them.”

“All you need for a lifetime of successful investing is a few big winners, and the pluses from those will overwhelm the minuses from the stocks that don’t work out.”

Be patient and much success in 2017!

[…] The Stock Trends for 2017, comprised of 21 handpicked stocks (discretionary style), is beating the major market indices by a healthy margin. The Nasdaq Composite is the closest but still trails by four percentage points. In order to be even, the Nasdaq would have to improve its year-to-date results (12.24%) by 30%. […]