We all know IBM gave investors an excellent return last year versus previous years but can the stock continue to move higher. Is this the new and improved sustainable Big Blue?

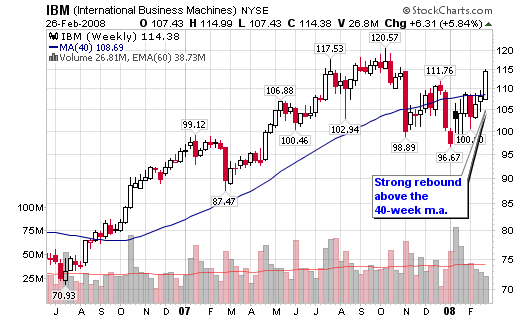

International Business Machines (IBM) has been making some of its largest gains of the past ten years, starting at the end of 2006. Not since the late 1990’s has the stock enjoyed this type of run with volume support which translates into a positive accumulation/ distribution rating.

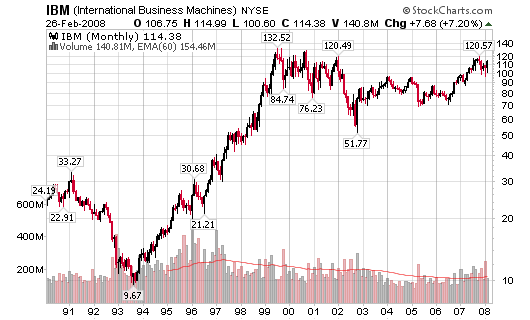

IBM went from a split adjusted price of $9.67 in 1993 to $132.52 at its peak in the 1999 bull market. It corrected to $51.77 in 2002 before trading sideways for the next four years. Something clicked in late 2006 and the stock ran-up from $70 to a high of $120.57.

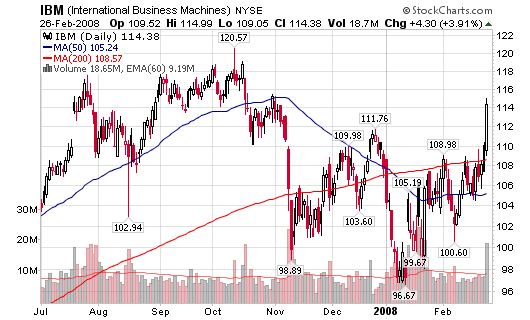

IBM closed at $114.38 Tuesday night, a 5.84% gain on volume 98% larger than the average. The stock crossed back above the 40-week (200-d) moving average while also jumping back above the shorter term 50-d moving average. An ascending triple top breakout has also flashed on the point and figure chart.

Next stop: Is it a new multi-decade high which signals a buy?

Institutional Numbers:

Total Held by Institutions: 2,947

Money Market: 1,357

Mutual Fund: 1,472

Other: 118

New Positions: 288

Positions Sold: 125

Shares Held: 1.26 Bil

Shares Held Previous Period: 1.23 Bil

Shares Bought: 116.2 Mil

Shares Sold: 89.5 Mil

Value of Shares Bought: $12.14 Bil

Value of Shares Sold: $9.36 Bil

26.7 million new shares have been bought (versus sold)

$2.8 billion new dollars have flowed into the stock

So what does IBM do these days?

IBM’s business comprises three principal business segments: Systems and Financing, Software and Services.

The majority of the Company’s enterprise business, which excludes the Company’s original equipment manufacturer technology business, occurs in industries that are broadly grouped into six sectors: financial services (banking, financial markets and insurance), public (education, government, healthcare and life sciences), industrial (aerospace, automotive, defense, chemical and petroleum and electronics), distribution (consumer products, retail, travel and transportation), communications (telecommunications, media and entertainment, and energy and utilities) and small and medium business (mainly companies with less than 1,000 employees).

Net Income:

2007: 10,419

2006: 9,492

2005: 7,933

2004: 7,479

2003: 6,558

Revenue has remained mostly flat while operating income and net income continue to rise.

P/E Ratio: 15.25x

PEG Ratio: 1.53x

ROE: 36.57%

ROA: 9.32%

ROI: 15.35%

Earnings:

FY 2009: $9.21E

FY 2008: $8.22E

FY 2007: $7.13

FY 2006: $6.06

FY 2005: $5.32

Earnings and net income are decelerating. there are better stocks out there.

IBM ignited a stock rally by announcing a $15B share buyback. IBM increased its full-year earnings guidance 5 cents to $8.25 due to stock repurchase.

Doug Kass calculates that IBM’s $15B share repurchasing should boost earnings by 60 cents [~6% reduction of shares]. So IBM must think its core business will contract in order to derive only a 5 cent boost in full-year earnings. Inquiring minds want to know what ugliness IBM sees coming this year.

If PMs and analysts that cover IBM see good business ahead. Then why only boost earnings

guidance by a nickel when $15B of repurchased shares would boost earnings by 60 cents? And what does this say about capex if IBM would rather repurchase shares with ~1.5 years of net income? How many jobs, new products, plants and techo breakthroughs will IBM’s repurchase program produce?

By the way IBM’s total debt increased 55.52% last year, to $35.274B from $22.682B in 2006.

a chart will fool someone all of the time

I’m an editor with Seeking Alpha, and would appreciate if you could contact me at your earliest convenience.

rbd,

What are you implying with the last statement? Not all stocks are for all people so don’t take shots at some of the readers like you are better than them.

By the way, numbers fool people more often than charts.

I’m implying that IMB’s numbers sucked. Research it. It’s not rocket science. IBM is in a lot of trouble.

Abby – seeking alpha sucks. Writers with bad information post everyday… its really sad…actually it’s pathetic… and everyone knows it. The information on there is not researched… its worse than hearsay. my e-mail is ryandbaird@gamil.com if you need to contact me. I couldn’t find you on seeking alpha. I hope you’re not one of the sad, un-researched authors on the site……….

rdb,

Cut the crap on my website. Take your problems with SeekingAlpha elsewhere, not here.

Big Blue is a technical buy on a new 52-week high. We trade; we don’t invest for the long term based on fundamentals that mean next to nothing in our methods. Learn what we do here before being a know-it-all wise guy.

My research and success speaks for itself over the past 4 years; I certainly don’t need to defend it

Chris your research is awesome. I love this site. I apologize if my comment was disrespectful to you in any way.