I started a mock portfolio on January 1, 2013, for fun, on stocktwits and twitter for the year 2013. I have owned and currently own several names but always clarified that I was not holding all 13 at any one time nor did I own every stock listed throughout the entire year. The purpose of the exercise was to develop a mock portfolio on social media which would be held for all 365 days without buy or sell rules to see if high quality growth stocks could outperform the general market without lifting a finger.

Well, SUCCESS:

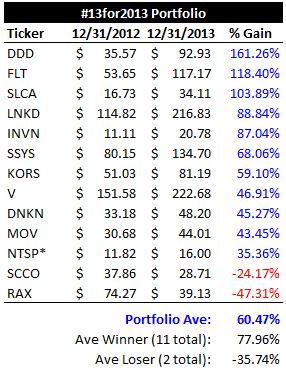

As it turns out, the 13 handpicked stocks easily outperformed the major indices with a whopping 60.47% gain vs. a 31.80% gain for the S&P 500. This mock portfolio essentially doubled the average of the S&P 500 for the calendar year 2013.

First tweet: #13for2013

10:04 PM – 1 Jan 13

13 Stocks for 2013: $SSYS $DDD $DNKN $RAX $LNKD $KORS $MOV $FLT $INVN $NTSP $SLCA $V $SCCO

Let’s take a look back as to why I selected these 13 stocks so we can use a similar strategy to select 14 stocks for 2014.

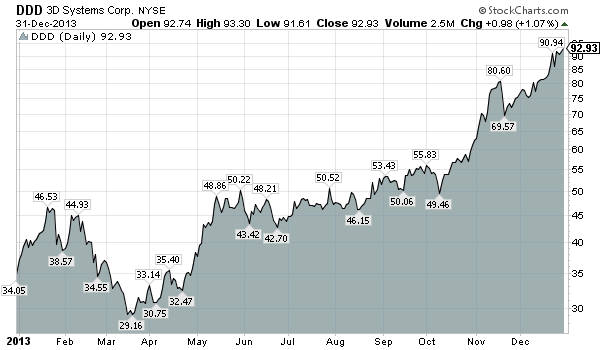

DDD – 3D Systems Corp.

The company manufactures and markets 3D printers, print materials, on-demand custom parts services, and 3D authoring solutions for professionals and consumers.

The entire 3D industry started to explode in 2012 and I felt the trend would continue strong into 2013. That thinking was correct as DDD led the portfolio with a 161.26% gain. I believe this industry is still within its infancy with room for further growth and will likely select at least one 3D stock in the 2014 portfolio. Many stocks within the group are extended so be careful with your selections and wait for pullbacks (low risk / high reward). Some analysts believe that this industry is “gimmicky” but I am not completely sold on that notion. The industry is young and the true leaders will take time to establish their position but I do believe 3D printing is here to stay (in one form or another).

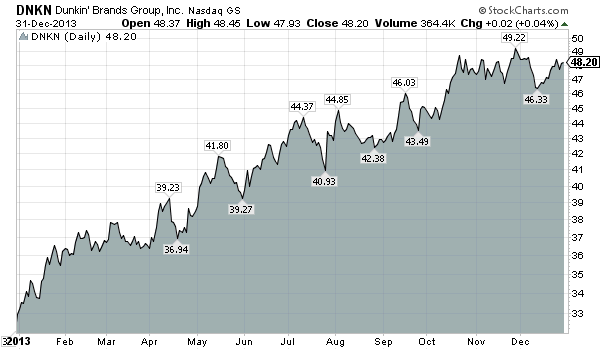

DNKN – Dunkin’ Brands Group, Inc.

Dunkin Brands Group, Inc., together with its subsidiaries, owns, operates, and franchises quick service restaurants under the Dunkin Donuts and Baskin-Robbins brands worldwide. The company has approximately 10,800 Dunkin’ Donuts restaurants; and approximately 7,000 Baskin-Robbins restaurants.

I liked the stock and still own shares today because those 10,800 stores are mostly concentrated in the north east. The company still has room for expansion which was my thought last year as the west coast is wide open, as well as international markets. This is a $60-$100 type stock over the long term based on Dunkin’s strong brand and loyal following. Even better, the stock pays a dividend. Bullish on this stock long term.

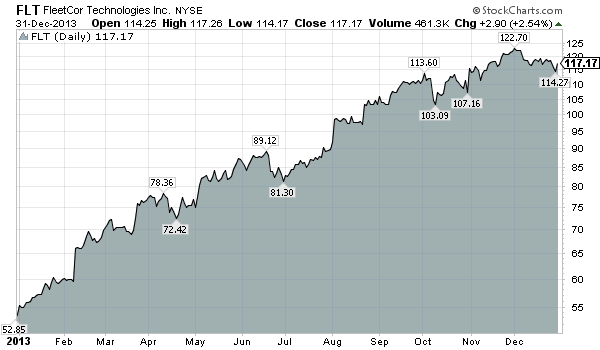

FLT – FleetCor Technologies, Inc.

FleetCor Technologies, Inc. provides fuel cards and workforce payment products and services to businesses, commercial fleets, oil companies, petroleum marketers, and government entities in North America, Latin America, and Europe. It sells a range of customized fleet and lodging payment programs; and offers various card products to purchase fuel, lodging, and related products and services at participating locations.

It’s a generic description from Yahoo Finance but that’s what caught my attention as this is such a great concept in a huge industry. The stock has had a heck of a two year run but can be considered for additional buys anywhere above the 200-d ma in the future. I am big supporter and buyer of “payment” solutions going forward (whether it is specialized in an industry or in general such as a credit card). I maintain my bullish outlook on this stock and the industry.

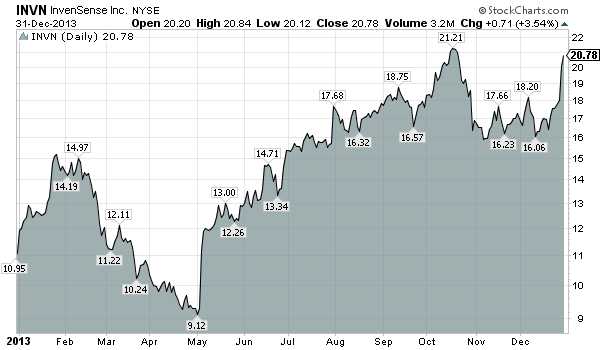

INVN – InvenSense, Inc.

InvenSense, Inc. designs, develops, markets, and sells micro-electro-mechanical system (MEMS) gyroscopes for motion tracking devices in consumer electronics. The company delivers motion interface solutions based on its multi-axis gyroscope technology that target smartphones and tablets, console and portable video gaming devices, digital still and video cameras, smart televisions, 3D mice, navigation devices, toys, and health and fitness accessories.

The key terms here are “wearables” and “sensors”. Just about everything we will use in the future will contain sensors to some degree so that is why I have been extremely bullish on INVN since 2012. It’s hasn’t worked out as smoothly as I wanted since my first purchase in 2012 but it has been profitable over the long term. The past year has been more profitable but it has also been extremely volatile. The stock made a strong late year push but needs to deliver consistent earnings to reduce the volatility. If it can do that, I can see this stock trading above $30 per share in 2014. I am still bullish on INVN going into 2014 and hold shares today (the entire industry is just beginning to explode).

KORS – Michael Kors Holdings Ltd.

Michael Kors Holdings Limited engages in the design, marketing, distribution, and retailing of branded women’s apparel and accessories, and men’s apparel. The company operates in three segments: Retail, Wholesale, and Licensing.

KORS caught my eye based on being a recent IPO, having a decent chart setup and the items lurking around my house – in the form of cloths and watches for my wife. I purchased several of those items so I went the Peter Lynch route: “Buy what you know”. I watch what my wife buys since the companies she likes (which trade publically) tend to do well over time (i.e.: SBUX, COH, CMG, AAPL, etc.). KORS was a big winner in 2013 and likely has room for success in the future. Although I am not a huge retail fan over the long term, if this one can hold support, it may have another run in it.

LNKD – LinkedIn Corporation

LinkedIn Corporation operates an online professional network. The company, through its proprietary platform, allows members to create, manage, and share their professional identity online; build and engage with their professional networks; access shared knowledge and insights; and find business opportunities. Its platform also offers members with solutions, including applications and tools to search, connect, and communicate with business contacts, learn about career opportunities, join industry groups, research organizations, and share information.

LNKD was the one social network that could show me how it makes money, in multiple ways with a sustainable model. That in addition to the fact that I use the network and see it has a higher quality community led me to add this stock based on a decent chart setup. The stock is currently basing and if it can hold support will offer an opportunity to jump aboard again in 2014 (multiples are high but that’s never stopped me before). I remain bullish on social media in 2014 (but it will likely be volatile).

MOV – Movado Group, Inc.

Movado Group, Inc. designs, sources, markets, and distributes fine watches. It operates in two segments, Wholesale and Retail. The company offers its watches under the Coach, Concord, Ebel, ESQ, Scuderia Ferrari, HUGO BOSS, Juicy Couture, Lacoste, Movado, and Tommy Hilfiger brands to jewelry store chains, department stores, independent regional jewelers, licensed partner retail stores, and a network of independent distributors.

I own Movado watches and love them so when I researched the company, the chart and the industry as a whole (retail was hot in late 2012), I decided to add it to the mix. It’s worked out well. Movado isn’t a high flyer like KORS but has given the patient investor respectable gains. I don’t see a need for owning this stock going forward (at this time).

NTSP – Netspend Holdings, Inc.

TSYS (TSS) acquired NetSpend (NTSP), a leading provider of general purpose reloadable (GPR) prepaid debit cards, for $16.00/share cash, or $1.4B, a 30% premium in 2013. NTSP paid out quickly as it was acquired for a healthy profit. I liked and still like the idea of pre-paid cards considering a large portion of the population lives paycheck-to-paycheck without decent credit.

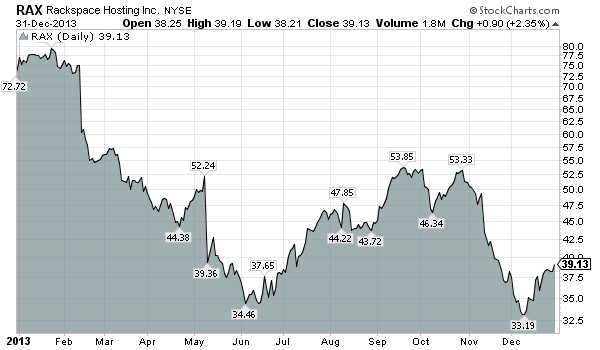

RAX – Rackspace Hosting, Inc.

Rackspace Hosting, Inc., through its subsidiaries, provides cloud computing services, managing Web-based IT systems for small and medium-sized businesses, and large enterprises worldwide.

RAX had its run in 2011 and 2012 only to fizzle out in 2013. I am a big believer in the cloud so I decided to add what I viewed as the independent leader in the category. This was one of two mistakes in the 2013 portfolio. I held the stock in the mock portfolio but in real life trading, sell rules would have had this stock eliminated long before the end of the year. I think big companies such as Amazon $AMZN, Apple $AAPL and Google $GOOG will control this space going forward.

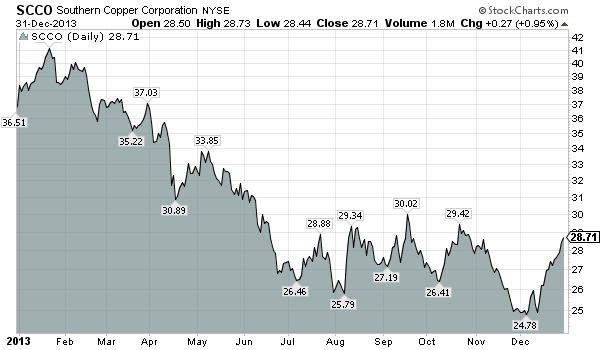

SCCO – Southern Copper Corp.

Southern Copper Corporation engages in mining, exploring, producing, smelting, and refining copper and other minerals in Peru, Mexico, and Chile. It is involved in the mining, milling, and flotation of copper ore to produce copper and molybdenum concentrates; smelting of copper concentrates to produce anode copper; and refining of anode copper to produce copper cathodes, as well as refined silver.

I swung and I missed on this one. I selected the stock based on a strong chart the second half of 2012, a strong dividend and positive future prospects. It will come back in the future but for now, I’ll stick to what I know rather than speculating on what I think I know (based on macroeconomic and commodity predictions).

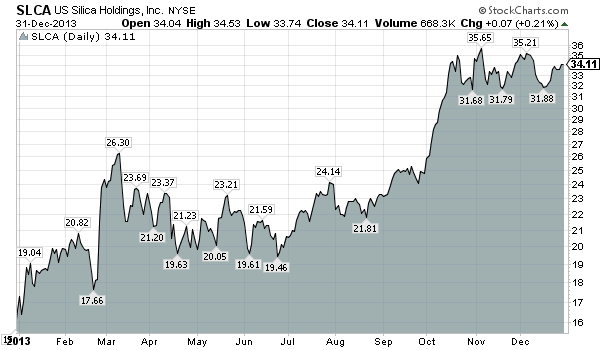

SLCA – U.S. Silica Holdings, Inc.

U.S. Silica Holdings, Inc., together with its subsidiaries, engages in the mining, processing, and sale of commercial silica in the United States. It operates in two segments, Oil & Gas Proppants and Industrial & Specialty Products. The company offers whole grain commercial silica products to be used as fracturing sand in connection with oil and natural gas recovery, as well as in various size distributions, grain shapes, and chemical purity levels for manufacturing glass products. It also provides ground commercial silica products for use in plastics, rubber, polishes, cleansers, paints, glazes, textile fiberglass, and precision castings; and fine ground silica for use in premium paints, specialty coatings, sealants, silicone rubber, and epoxies.

The main reasons for adding SLCA was the explosion in “fracking” in the US. Whether one views the fracking industry as evil or necessary, it is growing and silica is needed. What I don’t like about “fracking” is the fact that the US government can levy laws and restrictions that could adversely affect the stocks in this industry group. The stock is currently basing and could be setting up for additional gains in 2014. It may be worth the risk with a buy above a major moving average.

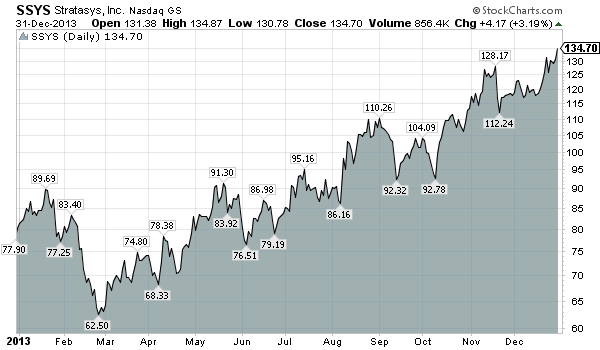

SSYS – Stratasys Ltd.

Stratasys Ltd. provides additive manufacturing (AM) solutions for the creation of parts used in the processes of designing and manufacturing products and for the direct manufacture of end parts. Its AM systems utilize its patented fused deposition modeling (FDM) and inkjet-based PolyJet technologies to enable the production of prototypes, tools used for production and manufactured goods directly from three-dimensional (3D) CAD files or other 3D content. The company offers desktop 3D printers for idea and design development, a range of systems for rapid prototyping, and production systems for direct digital manufacturing under the uPrint, Mojo, Objet, Dimension, Fortus, and Solidscape brands

Similar to DDD, I selected SSYS into the portfolio based on the growth potentials within the 3D industry. The stock has gone from $20 to $130 in just over two years with the trend continuing. It’s currently extended from an ideal entry point so wait for it to base and provide a lower risk / higher reward setup.

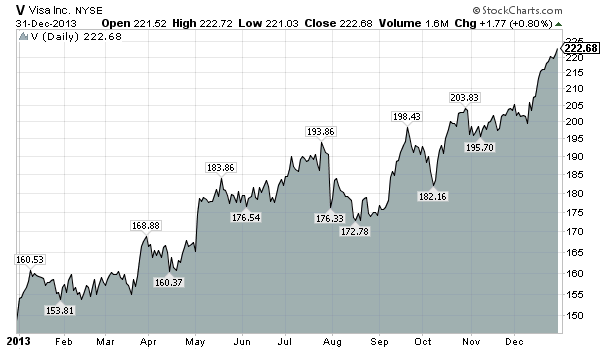

V – Visa Inc.

Visa Inc., a payments technology company, is engaged in the operation of retail electronic payments network worldwide. The company facilitates commerce through the transfer of value and information among financial institutions, merchants, consumers, businesses, and government entities.

I have owned the stock for two and a half years as of the end of 2013 and it has been my most consistent all-star throughout that time. Rather than give a detailed explanation here, please click this link to see all the reasons why I loved the concept in 2007 and still love it today:

As I highlighted in 2007, pre-IPO:

“Because it acts as an intermediary, Visa doesn’t sustain losses when consumers don’t repay the debts run up on credit cards bearing its brand. Those liabilities instead fall to the banks that issue the cards and set the terms of repayment”

There you have it – the results and thinking behind the #13for2013 portfolio. Based on the above logic, I will be selecting and publishing a #14for2014 portfolio on stocktwits and twitter tonight. I will follow that list with a detailed analysis, such as the above, as to why I selected the specific stocks. I will note that it’s been difficult to select a mock buy-and-hold list in 2014 due to the extended nature of the overall market. The goal again will be to outperform the S&P 500 by a wide margin.

Happy New Year and much success in 2014!

Congrats to your selection! They are wonderful. Though I did not take any from this list. I really enjoyed your thought process and methodology described here. I am looking forward to see your post for the first half of 2014.

Have a prosperous New Year!

Kevin

Thank you Kevin. To much success in 2014.