Making a Christmas List – Part II

I need to know where I am going by using a Garmin in the new Lexus LS that I am asking for. I don’t have GPS in any of the cars I own and I honestly don’t know why!

I feel that this technology is a necessity for every car on the road and have nothing but the best to say about the product after using it extensively in Hawaii (earlier this year). I found GPS to be very reliable while using a loaner car over the summer while venturing out to Pennsylvania for a friend’s wedding. I would have been lost without a Garmin and always feel so secure when traveling with the unit.

I find the products to be competitively priced for an ideal holiday gift.

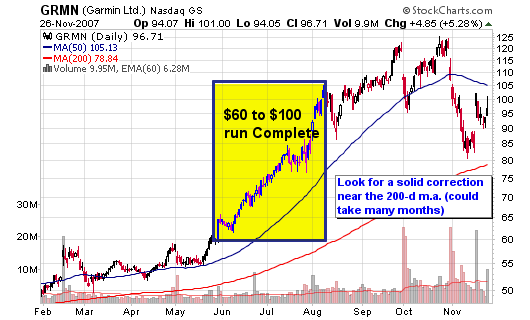

Garmin (GRMN) is up about 900% since its debut as an IPO during the past seven years. The stock peaked earlier this year with a 1,126% gain since the IPO. It more than doubled in 2007 before consolidating during the current pullback towards the 200-day moving average.

Garmin took off in May 2007 after crossing the $60 level , successfully completing the $60-$100 run in less than three months.

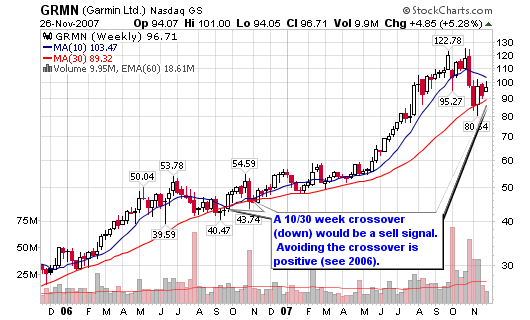

Garmin was a stock I owned earlier this year and is one that I would not hesitate to buy again based on its leadership status but right now is not the right time based on pure technical analysis.

I am looking for a solid base formation at or near the 200-day moving average that could take months to develop (be patient). Look back and you can see that the stock traded sideways for many months before blasting to new highs in the second half of 2007. I can’t setup the proper risk/reward strategy until I can see a base and/or change in the current short term down-trending correction. I will watch and revisit this stock if and when the ideal buying opportunity presents itself.

Earnings Watch:

FY 2005: $1.37

FY 2006: $2.35

FY 2007: $3.55E (looking for a 51%+ increase over last year)

FY 2008: $4.36E

FY 2009: $4.99E

ROE: 43%

ROA: 42%

P/E: 29x

PEG: 1.47

Institutional Analysis:

Total Institutions: 585

Money Market: 306

Mutual Fund: 254

Other: 25

Shares Held: 117.86 mil

Shares Held Previous Period: 106.89 mil

Shares Bought: 24.09 mil

Shares Sold: 13.12 mil

Value of Shares Bought: $2.8 Bil

Value of Shares Sold: $1.5 Bil

Garmin (GRMN) Coverage on the blog:

- Should we Accumulate Shares?

GRMN – 82.32, the former high flyer is down $40 as it approaches the 200-d m.a. for the first time since early 2007. A base here is a great accumulation opportunity.

- Tracking Garmin (GRMN)

- Indicators and Research Save me Money

I saved the portfolio $4,000 in profits from my sales on Friday and Monday (GRMN and SLW).

- Support at the 200-day Moving Average

GRMN – $49.69 -sitting on the 200-day moving average!

- Ten Stocks to Watch

GRMN – $47.18 ($95.35) down over 2% for the week but the stock continues to hold the 50-d m.a. as support while maintaining a presence near the psychological triple digit threshold. I still like the stock in a rallying market (could make a nice option play for a solid run).

- MSW Market Overview

Looking at the MSW Index, we see that every stock fell for the week, so which ones dropped the least?

GRMN: -1.75%

TS: -2.71%

GRMN – $49.12 ($99.26), These were the only qualifying stocks from the MSW Index that fell less than the major indexes. Garmin (GRMN) fell less than every major market index and found support near $95 and the 50-day moving average. It did qualify for distribution, the first in 13 full weeks. - Interesting Stocks with 15% of a New High

GRMN – $31.88 ($64.42), flirting with the 50-d m.a. as the stock sits in the $60 range but is not a an official $60-$100 candidate until it can breakout above the recent peaks set at $70.07 and $68.88

Christmas List Series:

Next up in this 5-part Series:

- Part III: A New Suit from The Men’s Warehouse (MW)

Future Wish List Items:

- Part IV: A Video iPod from Apple (AAPL)

- Part V: A Blackberry Pearl from Research in Motion (RIMM), using the Verizon Wireless (VZ) Network

Connect with Me